A glance at the retail fundamentals in Florida reveals a dramatically different retail scene from market to market.

What the different markets in the state have in common is that a low amount of new construction will ease pressure on rents everywhere. The lack of new supply will help keep vacancies under control and help keep rents from falling further. In fact, in Miami, rents have actually increased slightly in 2010.

The other commonality in Florida's markets is the question of unemployment. Throughout the state, unemployment rates are hovering at or above 10 percent. That is casting a pall over the retail picture in many markets.

Still, while things are not improving anywhere, there are signs that markets have at least bottomed out and have either begun to recover or are poised to improve in the near future.

Here's a glimpse of CB Ricard Ellis' second quarter findings in South Florida, Jacksonville, Orlando and Tampa.

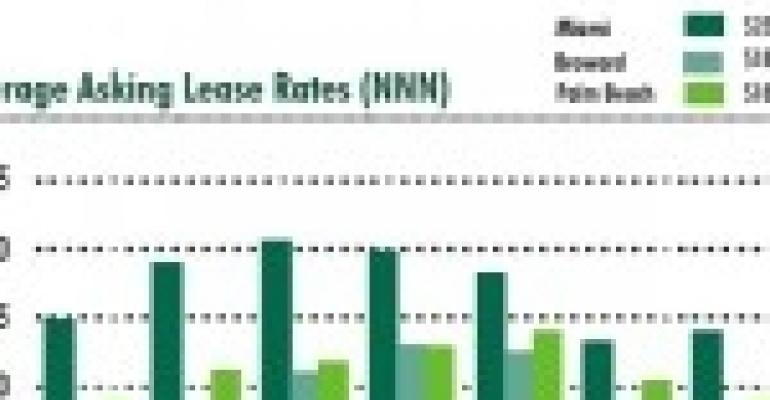

South Florida

For example, South Florida--which includes Miami-Dade, Broward and Palm Beach Counties--remains relatively robust. Rents have fallen from peaks hit in 2006, but not dramatically so. In fact, rents in Miami have actually begun to tick upwards in 2010. Rents have risen $0.88 per square foot from 2009 to $23.90 per square foot. That means rents in the county are down about 21 percent from the 2006 peak of $30.45 per square foot. Rents in Broward and Palm Beach Counties are down 13 percent from the peak of the market.

According to CBRE's report:

"The basic fundamentals of the region, such as demographics and continued influx of seasonal residents from the Northeastern portion of the United States, keeps the retail market competitive. Development of new product in the tri-county area has dropped with now new product currently under construction. This, coupled with small signs that the economy is stabilizing, should help keep vacancies from rising drastically over the next twelve months."

At 5.4 percent, Miami-Dade County has one of the lowest vacancy rates in the entire state. The vacancy rate is more than double that in Broward County at 12.5 percent and only slightly better in Palm Beach County at 11.4 percent. As a whole, the vacancy rate on South Florida's more than 130 million square feet of retail space stands at 8.9 percent with average asking rates coming in at $20.06 per square foot.

Jacksonville

The picture changes when you get to Jacksonville. According to a report written by Cliff Taylor, a first vice president with CBRE, Jacksonville's retail market exhibited mixed signals in the second quarter of 2010.

The direct vacancy rate increased to 10.6% while the total vacancy increased to 11.0%. While these movements are rather small, they speak more clearly to the current state of the retail market in Jacksonville. Small pockets of geography are seeing positive movement in isolation and limited new development is being received in a positive way. However, for the vast majority of the market, tenants remain hard to come by, space remains dark for extended periods and no impetus for rental rate growth appear on the horizon.

One factor weighing on the region is the fact that the unemployment rate in the Jacksonville MSA counties remains high. The unemployment rate is 11.4 percent in Duval County, 10.4 percent in Nassau County, 10.1 percent in Clay County and 9.2 percent in St. Johns County.

Average area rents stand at $15.66 per square foot. By property type, rents are $13.85 per square foot for neighborhood centers, $16.37 per square foot for community centers and $19.51 per square foot for regional centers, according to CBRE's stats.

Construction activity remains at a minimum in the market, which should help going forward. Overall, there are no new developments under construction and just three properties completed construction during the quarter containing 415,894 square feet. Of that, 351,332 square feet was occupied.

Orlando

Moving to Orlando, the picture changes again. There, activity has remained "steady", according to CBRE. The beginning of the year showed an improvement in leasing. And overall the vacancy rate is fairly low at just 7.3 percent. Leasing rates, however, have fallen in 2010 in comparison with 2009 from $17.06 per square foot to $16.87 per square foot.

The picture is similar in the three main counties surrounding Orlando. In Orange County the vacancy rate is 7.5 percent and average rents are $17.17 per square foot. In Osceola County the vacancy rate is 6.5 percent and average rents are $18.10 per square foot. And in Seminole County the vacancy rate is 7.1 percent and average rents are $16.14 per square foot. The unemployment rates in the three counties are 11.1 percent in Orange, 12.0 percent in Osceola and 10.5 percent in Seminole.

Like in other Florida markets, construction is minimal. There is just 172,373 square feet of new retail space in the region and no space has been delivered year to date.

According a market report compiled by CBRE Senior Associate Jorge Rodriguez:

Rent concessions and free rent are still relevant for multi-year deals with qualified retailers. Landlords need to pay attention to tenant retention strategies, plug-vacancy at reasonable costs, and maintain shopping centers in top-notch condition. The current economic challenges we are facing make it even more important than ever for tenants to consider the strength and capacity of their respective landlords. As tenants, they should be extremely aware and concerned about who they execute leases with. The current economic conditions will continue to place many developers in difficult positions with limited exit choices. The importance of qualifying the true soundness of their potential landlords has and will continue to be an important analysis for retailers.

Tampa

Tampa fared the worst in the second quarter posting negative absorption of 296,000 square feet because of closings by major retailers. Small shop leasing helped, however, posting positive absorption of 26,000 square feet.

Despite the net absorption, the vacancy rate in Tampa stands at a relatively low 7.7 percent. Average asking rents fell 3.2 percent to $14.67 per square foot from the first quarter.

According to CBRE's report:

Despite the negative absorption, retailers remain cautiously optimistic that the worst is behind them as they look to resume expanding albeit at a slower pace....

Retail professionals are confident we are approaching bottom, although more downward pressure on effective rents and space consolidation is still being felt across Tampa Bay.

By property type, Tampa's 10 regional malls are the healthiest properties. The vacancy rate at those properties stands at 1.5 percent with asking rents at $28.00 per square foot. The vacancy rate at freestanding retail spaces is 3.7 percent with rents at $5.23 per square foot. The market's 18 power centers also have high occupancies with the vacancy rate at 5.7 percent and rents at $19.31 per square foot. The 232 neighborhood centers have a vacancy rate of 9.7 percent and average rents of $15.21 per square foot. Finally, the 156 community centers in the Tampa region have the highest vacancy rate--at 11.2 percent--and average rents of $14.82 per square foot.

There are no new retail centers under construction in the Tampa market and no new projects were completed in the second quarter.