CBRE Econometric Advisors (CBRE-EA) is forecasting that the availability rate for neighborhood, community and strip centers will decline to 12.7 percent by the end of 2011. The ongoing pick-up in retail sales, combined with limited supply, will slowly decrease the national availability rate for neighborhood and community centers.

CBRE-EA plans to release the findings on Wednesday, May 11, but provide Retail Traffic with a sneak peek at its projections.

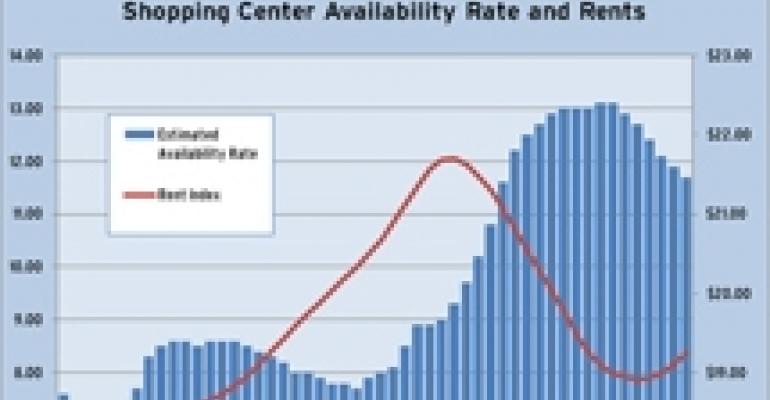

The availability rate (which CBRE defines as space that is actively being marketed and available for tenant build-out within 12 months) stood at 13.1 percent at the end of the first quarter—the highest level in the past decade. During the quarter, the industry posted negative net absorption of 1.32 million square feet on the total shopping center supply of approximately 1.72 billion square feet.

CBRE Econometric Advisors is projecting the availability rate to remain flat in the second quarter before improving in the third and fourth quarters and all through 2012. The outlook estimates that net absorption will steadily rise in the next seven quarters starting with 2.35 million square feet in the second quarter and growing to 6.37 million square feet by the fourth quarter of 2012.

As a result of the improving occupancy picture, rents—which have decline every quarter since the second quarter of 2008—will finally turn beginning in the first quarter of 2012. As of the end of the first quarter, rents stood at $19.09 per square foot—down from a peak of $2.70 per square foot in the first quarter of 2008. CBRE-EA projects rents will continue to slide and bottom at $18.92 per square foot in the fourth quarter of 2011. After that, rents will begin to rise and reach $19.25 per square foot by the fourth quarter of 2012.

“While high availability will keep pressure on rents until next year, demand for space is positive for the first time since 2007,” CBRE-EA Economist Abigail Rosenbaum said in a statement. “Annual supply growth for neighborhood and community centers is only expected to amount to 1 percent annually during the next few years —well below its level between 2000 and 2008 prior to the downturn. This combination will provide rent growth momentum for ‘necessity’ focused retail centers.”

Markets expected to achieve strong future rent growth include Denver, Nashville, Houston, Austin and Washington, D.C.

CBRE-EA is the latest firm to chime in on the state of retail real estate fundamentals. CoStar recently issued its issued its first quarter report, which measured the overall retail vacancy rate at 7.1 percent while in mid-April, Reis Inc. the vacancy rates at regional malls hit 9.1 percent and at shopping centers remained at 10.9 percent.