A new report from the Mortgage Bankers Association (MBA) shows that commercial mortgages have performed better than other types of loans over the course of 2010 for banks and thrifts.

MBA estimates that commercial mortgages, which make up $1.1 trillion or 15 percent of banks’ overall loan holdings, finished the year with lower delinquency rates than other types of loans. And over a four-year period the sector has accounted for less than 5 percent of bank and thrifts total charge-offs.

At the end of 2010, the 30+ day delinquency rate for commercial mortgages reached 5.33 percent, compared to the 6.48 percent rate for all loans. (The report also looks at multifamily mortgages, commercial and industrial loans, construction loans, credit card debt and loans to individuals). Moreover, the figure declined more than 30 basis points from 5.64 percent at the end of 2009. Construction loans, on the other hand, had the highest 30+ day delinquency rate of any loan type, at 17.98 percent.

MBA also examined charge-off rates for various loan types, which measure the banks’ assessment of the share of outstanding loan balance they are unlikely to get back. Here once again, commercial mortgages fared better than other loan types. In 2010, banks and thrifts charge-offs rates for commercial mortgages amounted to 1.36 percent. In contrast, the charge-off rate for credit card loans was 7.41 percent.

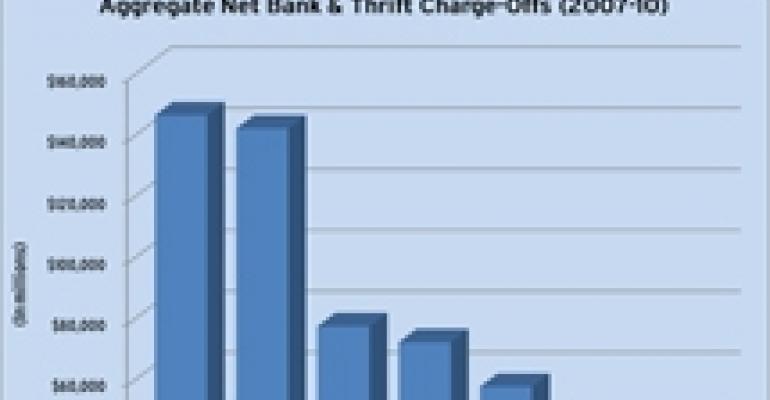

In fact, over a three-year period starting in 2007 and encompassing the credit crunch and the recession, banks and thrifts charged off only $25.9 billion on commercial mortgages, accounting for 4.96 percent of total bank and thrift charge-offs. During the same period, the charge-offs for single-family mortgages totaled $145.3 billion, accounting for 27.8 percent of the total, and the charge-offs for credit card loans $141.0 billion, making up 27.0 percent of the total. Charge-off on construction loans totaled $71.0 billion—or 13.6 percent of the total.

“Like other parts of the economy, the performance of commercial and multifamily mortgages has been negatively impacted by job losses, consumer restraint, manufacturing declines and reduced household formation,” the report said. “When compared to other parts of the economy and other types of loans at banks and thrifts, however, the relatively stable performance and low charge-offs of commercial and multifamily mortgages have been a net positive to these institutions through the recent recession.”

To be sure, the report did not look at CMBS loans, which have experienced higher rates of delinquencies than those held by commercial banks or thrifts during the downturn. In addition, losses on commercial real estate loans have continued to help cause bank failures at local and regional banks throughout the country.