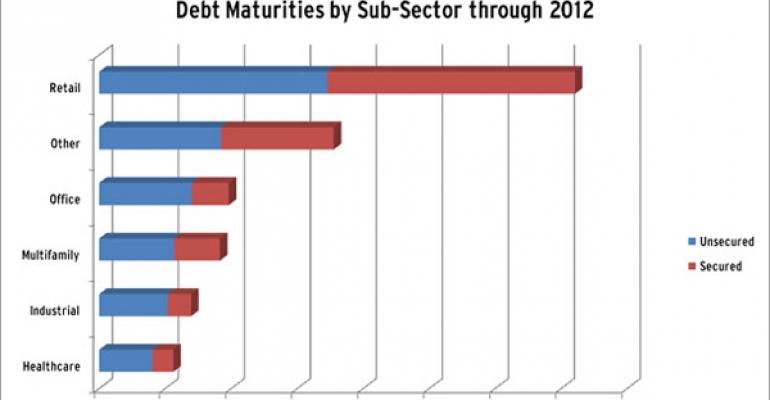

A new commercial real estate update from J.P. Morgan shows that publicly traded retail REITs face the greatest level of debt maturities coming due between now and 2012 out of all the REIT sectors. As of October, retail REITs have more than $36.0 billion in debt scheduled to come due through 2012, including $17.3 billion in unsecured debt and $18.8 billion in secured debt. By contrast, publicly traded office REITs, the group with the second greatest level of near-term maturities, face $9.8 billion in debt coming due through 2012, including $7.0 billion in unsecured debt and $2.8 billion in secured debt.

The REIT sector with the least amount of debt maturities is healthcare. Healthcare REITs have $6.5 billion in debt scheduled to come due between now and 2012.

Overall, J.P. Morgan estimates that the REIT industry will experience a gradual increase in debt maturities over the next three years, with the peak occuring in 2012, when $30.5 billion in debt will come due, including $20.9 billion in unsecured debt and $9.7 billion in secured debt. After that, REITs' annual debt maturities will level off, declining to $21.1 billion in 2013 and $9.3 billion in 2014.

In 2009, publicly traded REITs faced approximately $6.5 billion in debt maturities.