No relief is in sight for commercial property owners in Las Vegas.

While the tourism, gaming and hospitality industries are stabilizing, the near-term outlook for the Las Vegas economy remains bleak. Economic factors that affect real estate value, such as demographics, employment, income and housing, portend minimal growth in the next 12 to 24 months.

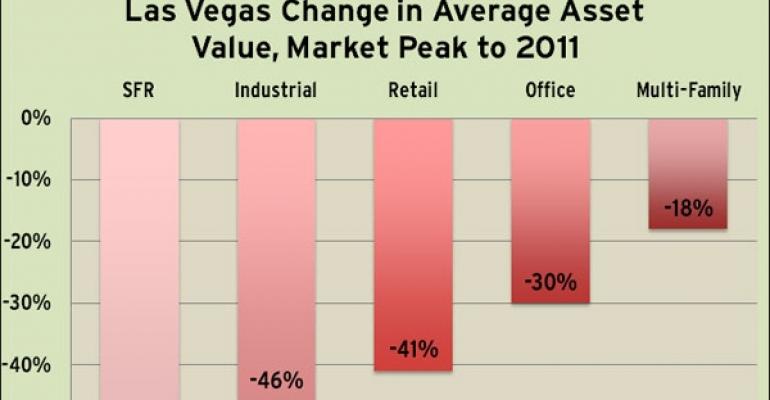

Business leaders’ confidence in the Las Vegas economy has turned pessimistic and continued its downward slide throughout 2011. The Southern Nevada Business Confidence Index, which measures companies’ outlook, fell to 99.91 for the fourth quarter, down from 99.96 in the third quarter. Adding to commercial property owners’ woes, real estate values for all asset classes are at historic lows. Property owners want to know if the steep decline in market values since the peak in 2008 will be reflected in the 2012-13 property tax assessments.

Taxpayers will soon find out: Clark County’s issuance of property tax assessments takes place in early December. When assessments arrive, property owners will need to evaluate the benefit of filing a property tax appeal.

Tragically, few owners will file an appeal, even though, on average, property taxes account for 33 percent of real estate operating expenses. They will simply pay their tax bills based on the belief that their assessment is reasonable and that challenging an assessment is too expensive, complicated and time-consuming.

However, rather than taking an immediate pass on contesting an assessment, Las Vegas property owners should consider the following points and then decide whether an appeal may be beneficial.

Long-term Benefits: For savvy taxpayers, the next few years represent a unique opportunity to reduce long-term tax liability. Because of Nevada’s partial abatement law or tax cap, a successful appeal this year will yield tax savings now and in the future. When property values begin to appreciate, the tax cap will limit the annual increase in tax liability to no more than 8 percent over the prior year.

Recapture Tax: Taxpayers must be careful to sidestep Nevada’s recapture tax. Even if a property’s taxable value declined last year, Nevada’s recapture provision applies if a property’s taxable value decreased by more than 15 percent between tax years 2010-11 and 2011-12, but increases by 15 percent or more in the upcoming 2012-13 tax year. If the recapture applies, the amount of tax that would have been collected without the tax cap will be levied on the property.

The Law on Value: It is important to understand how assessors value property in Nevada to evaluate if a property is overvalued. Owners may believe the taxable value appears reasonable based on their understanding of market value in the business world. But market value in the business world is different from market value for property tax purposes. Nevada law requires assessors to determine taxable value based on value in use rather than highest and best use. In many key instances, these two value concepts produce radically different values.

The Cost Approach: Nevada law requires assessors to determine the initial value of all property using the cost approach, which measures the current replacement cost of the improvements minus depreciation, plus the value of the site. The cost approach is limited in its application and is rarely used by investors to determine market value. In a depressed real estate market, the cost approach generally yields a result that exceeds market value unless all forms of accrued depreciation are deducted.

Value the Sticks and Bricks: Market value for property tax purposes is restricted to the valuation of the real estate alone, or the “sticks and bricks.” Nevada law prohibits the inclusion of personal property or intangible property in the assessor’s valuation. This applies particularly to businesses such as hotels and motels, assisted living and nursing facilities, and shopping centers and malls, which derive significant income from personal property and intangibles such as trade names, expertise and business skills.

Deadlines and Procedures: Owners should start planning an appeal before tax notices are mailed. The property tax appeal timeline is highly compressed in Nevada. Tax notices are mailed in early December, and this year taxpayers have until Jan. 17 to file an appeal. This leaves taxpayers with only about 30 days after receiving the tax notice to determine whether an appeal is warranted.

Where to Begin: Owners unfamiliar with the deadlines, procedures, and valuation methods used to arrive at their assessment can easily miss an opportunity to reduce their tax bill. To maximize the chances for success, an owner should consult with a tax professional or property tax lawyer with a sound knowledge of Nevada property tax law, valuation theory and tax assessment practices to identify potential avenues for reducing tax liability.

Douglas S. John is an attorney in the Tucson, Ariz. law firm of Bancroft & John, P.C. and a Nevada and Arizona member of American Property Tax Counsel, the national affiliation of property tax attorneys.