Although delinquencies on loans contained in commercial mortgage-backed securities (CMBS) seem to rise with each passing month, not all property types, loan vintages and markets are going through the same experience.

With retail properties in particular, the greatest problems are showing up in housing markets that went bust and areas where manufacturing has been hard hit in recent years, according to New York-based Trepp LLC. Moreover, loans issued in 2006 and 2007 are going bad at a higher rate than loans of other vintages.

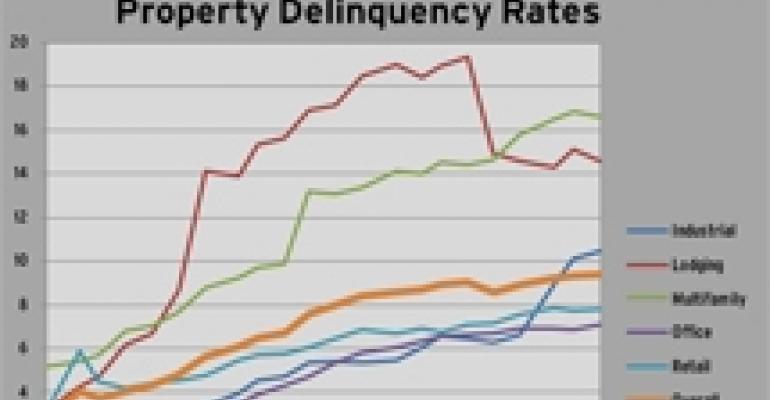

Overall, Trepp measured the national CMBS delinquency rate at 9.39% at the end of February. That represented a new record — topping January’s figure by five basis points. By property type, the multifamily sector had the highest delinquency rate (16.6%), followed by lodging (14.6%), industrial (10.4%), retail (7.8%) and office (7.1%).

Retail Traffic Editor-in-Chief David Bodamer spoke with Thomas Fink, senior vice president and managing director at Trepp, about trends the firm is seeing for retail properties that are ending up with delinquent CMBS loans.

Bodamer: Can you talk about how retail compares with the other major property types?

Fink: We have some 24,000 retail properties in the pool we monitor, so that gives us a good selection to look at across the entire marketplace. Overall, retail properties are doing better from a delinquency-rate perspective than a lot of other properties, which might surprise a lot of people. Multifamily is the worst right now and retail is actually better than the overall average.

Bodamer: Are there certain areas where the delinquency rate on retail properties is higher than others?

Fink: To a certain extent, there are not any huge surprises. Nevada leads because of the strain in the casino-related retail space. Alabama, believe it or not, is in the top 10 along with Arkansas, Arizona, Iowa, Louisiana, Colorado, Michigan, Ohio and lowly Vermont. In Vermont, there are not a lot of properties, so it could be a small-state influence. One bad loan can throw off the entire picture.

California has a lot of delinquent loans because of its size, but the delinquency rate there is just 6.9%.

Overall, looking at the numbers, you can see that it’s a lot of states with housing problems and a lot of states with issues in manufacturing. Both of those situations tend to create problems for retail as well. These are projects that were built in anticipation of residential development that never followed.

Bodamer: What about vintage? Or delinquencies concentrated in any particular years?

Fink: We do see that in the 2006 and 2007 vintage, there’s a lot more stress than you would expect for loans so recently originated. The retail delinquency rate is 10.5% for 2006 and 8.4% for 2007. There are also some problems with some older vintage loans as well. A lot of the loans from 1999 and 2000 have been paid off or refinanced. So, the stuff that’s left are where the problems exist and are showing delinquency rates in the middle teens overall. For 1999, where there’s about $1 billion in loans left, the delinquency rate is 24 percent. So that’s an interesting situation we’re running into.

Bodamer: What’s the reason the 1999 vintage of CMBS retail loans is showing signs of trouble?

Fink: Some of these might be older malls that have gotten to the end of their life cycle and gone into default. You expect them to have an issue, not because the borrower doesn’t like the property or because it’s a bad borrower. But for older centers sometimes the location is not what it was when the property was built. The population shifts. Or malls that were the center of the universe when they were built are seeing spotty traffic today. There might be new highways, or people have moved. Or there’s newer competition. It just might be the case that there isn’t much that can be done. The property is just at the end of its life cycle.

Bodamer: Is the pace of CMBS loans entering delinquency slowing? What can we expect going forward?

Fink: The overall pace of delinquencies is slowing, but that’s not necessarily true for retail. We’re still seeing a bit of an increase going into it.

Bodamer: Are there trends in how distressed retail situations are being resolved?

Fink: We’ve tracked about $20 billion of modifications since the start of 2010. Of that amount, about 45% have been retail properties. What we see is a combination of loan extensions for maturing loans and changes in amortization — lenders offering interest only for a while as well as some interest rate reductions, but not as much as you’d think. In most of these situations it’s a cash-flowing property, and the owner is committing additional capital, so the owner is able to work something out with the lender.