CMBS delinquencies dropped sharply in November after rising the previous two months, but it may be the last good news for a while as researchers expect that as 2007-vintage loans mature further delinquencies will set in.

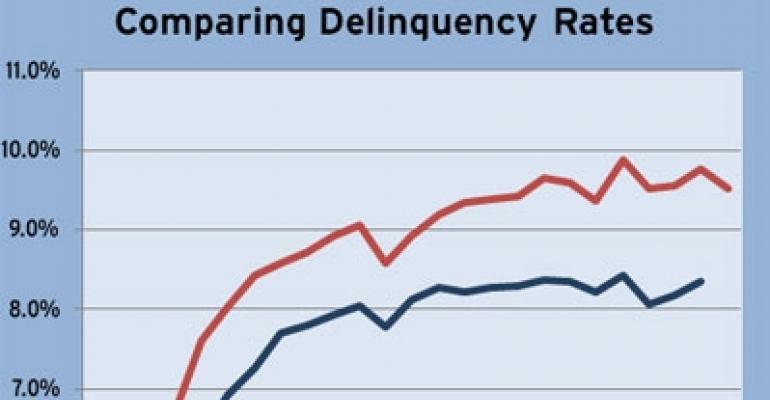

Two outlets that specialize in monitoring CMBS delinquencies, Trepp and Morningstar, each issued reports last week with Trepp’s report updated through November and Morningstar’s review covering through the end of October. Through October, Trepp reported the CMBS delinquency rate at 9.77 percent—the second highest point on record trailing only July’s figure of 9.88 percent. Morningstar, meanwhile, said the delinquency rate had hit 8.35 percent in October. Both firms measured rates rising in September and October after having fallen in August. In addition, Trepp’s latest report showed that the delinquency rate dropped 26 basis points to 9.51 percent in November.

Through October, Morning star reported the unpaid balance for specially serviced CMBS under review increased on a net basis by $974 million, up to $85.35 billion from $84.37 billion in September 2011. Newly transferred specially-serviced loans totaled 176 with an unpaid balance of $3.88 billion in October. The percentage of loans in special servicing in October by unpaid balance grew to 11.63 percent from 11.46 percent a month prior.

Trepp’s outlook

The 26-basis point decline in November was the second biggest drop in 2011, according to Trepp, surpassed only by August’s 36-point decline. The rate has now fallen in four of eleven months in 2011, according to the firm. The percentage of loans seriously delinquent (60+ days delinquent, in foreclosure, REO, or non-performing balloons) is now 8.88 percent, down 33 basis points for the month.

Going forward, however, Trepp sees trouble.

According to its report, “The day of reckoning is here for the class of 2007 originated loans as the five-year balloon loans that were made at the height of the commercial real estate bubble have begun to mature. The 2007 vintage was the weakest in terms of underwriting standards and it is widely expected that many of these loans will have trouble paying off at their balloon date. In total, about $15.5 billion of these loans will come due in 2012, with the majority reaching their balloon dates over the next six months.”

To put that in context, Trepp pointed out that in 2011, $13.7 billion in 2006-vintage five-year balloon loans reached their maturity date. Of that amount, $9.9 billion remains with almost 60 percent of that volume in special servicing and 45.9 percent are currently delinquent. In addition, another 8 percent are past their balloon date, but only making current interest payments while 22 percent have stopped making interest payments altogether.

So far, 27 percent of 2007 five-year loans are in special servicing and 18.5 percent are currently 30 or more days delinquent. Trepp expects those numbers to increase dramatically as 2012 plays out.

In addition to the question of 2007-vintage loans, Trepp expects the recent drop on new CMBS issuance to put pressure on delinquency rates. “Over the last year, the new CMBS issuance had the effect of increasing the denominator in our calculations. With new issuance effectively petering out after June, this helpful impact is now gone,” Trepp wrote.

By property type, Trepp reported that the hotel delinquency rate fell 184 basis points in November and now stands at 12.28 percent; the industrial delinquency rate rose 61 basis points and is at 12.20 percent; the office delinquency rate dropped 19 basis points to 8.76 percent; and the multifamily delinquency rate fell 55 basis points to 16.18 percent and the retail delinquency rate fell 9 basis points to 7.52 percent.

Morningstar’s perspective

Morningstar, meanwhile, updated its numbers through the end of October. According to the firm, the delinquent unpaid balance for CMBS increased by $1.06 billion in October 2011, up to $61.27 billion from $60.22 billion a month prior (reflecting a small 1.7 percent increase). This followed the previous month’s increase of $1.29 billion in September 2011 (a 2.2 percent increase). For 2011 year-to-date, the delinquent unpaid balance for CMBS continues to fluctuate on a monthly basis. The total unpaid balance of CMBS stands at $734.17 billion.

The resultant delinquency ratio for October 2011 of 8.35 percent is up from 8.18 percent a month prior and is still almost 30 times the Morningstar recorded low point of 0.283 percent in June 2007.

The delinquent unpaid balance in October 2011 is also up 3.5 percent from last October and remains over 27 times the low point of $2.21 billion in March 2007.

As a whole in October 2011, the distressed categories of 90+-day, Foreclosure and REO increased in aggregate by $939 million, following a $641 million decrease in September 2011, according to the firm. These figures had declined in three of the six previous reporting periods. Delinquent activity was also directly affected by another $1.28 billion in liquidations reported for October 2011 across 128 loans, at an average severity of 48.8 percent.

In addition, all deals seasoned at least a year had a total unpaid balance of $668.55 billion, with $61.27 billion of this balance being delinquent, reflecting a 9.17 percent delinquency rate. That is up from 8.94 percent in September and 8.96 percent six months ago. When agency CMBS deals are removed from the equation, deals seasoned at least a year had a total unpaid balance of $626.4 billion, with $61.23 billion of this balance being delinquent, reflecting a 9.76 percent delinquency rate up from 9.51 percent a month prior and 9.47 percent six months ago).

Looking forward, Morningstar expects “if the credit markets do not recover sufficiently to handle the upcoming balloon maturity risk in existing CMBS, or additional distressed loans already on the watchlist experience default, we could easily reach this level. … By property type, the greatest future risk exposure by unpaid balance is found in office collateral, while retail collateral is by far the largest by loan count.”

By property type, office surpassed the multifamily sector as the greatest contributor to overall CMBS delinquency. Delinquent office loans equate to 2.2 percent of the CMBS universe and 26.1 percent of total delinquency (up slightly from a month prior), with a delinquency rate of 8.3 percent (up from 7.8 percent a month prior).

Delinquent multi-family loans equate to 2.1 percent of the CMBS universe and 25.1 percent of total delinquency (down from a month prior), with a delinquency rate of 8.8 percent (down from 9.2 percent a month prior).

The total delinquency rate for CMBS hotel loans has shown some volatility the trailing-12 months. After starting the year at 14.3 percent, this rate fell to only 11 percent in September 2011. Through October 2011, however, the rate grew to 12.3 percent.