Two steps forward, one step back. That’s a fitting description for the performance of the commercial mortgage-backed securities (CMBS) market as a whole over the last three months.

After receding in May and June, the delinquency rate for securitized loans 30 days or more past due or in foreclosure climbed 51 basis points in July to reach 9.88%, according to New York-based Trepp LLC. It’s the highest delinquency rate in the history of the CMBS market.

New reporting standards implemented by some special servicers accounted for much of the increase, emphasizes Trepp. For example, if a special servicer is considering a possible loan modification, it is now standard practice for the servicer to also simultaneously initiate the foreclosure process to expedite matters in the event that the modification doesn’t occur.

This “dual tracking” approach, which includes foreclosure as a workout strategy, drives up the delinquency rate.

The rise in the July delinquency rate likely would have been higher than 51 basis points had it not been for the disposal of troubled loans (typically at a loss). The loan resolutions shaved the delinquency rate by an estimated 21 basis points.

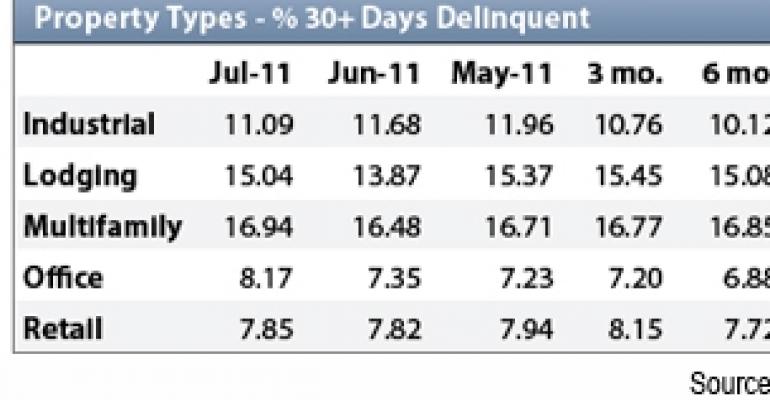

Among other highlights from Trepp’s report on the performance of the CMBS market in July:

• The percentage of loans seriously delinquent, defined as 60 days or more past due, rose 39 basis points over the prior month to 9.14%.

• The delinquency rate for office loans 30 days or more past due spiked 82 basis points to reach 8.17%, breaking the 8% threshold for the first time (see chart).

• The hotel delinquency rate soared 117 basis points to reach 15.04%.

• The industrial sector was the only property type to experience a decline in the delinquency rate, falling 59 basis points to 11.09%.

• The multifamily sector remains the worst performing property type on the CMBS front with a delinquency rate at nearly 17%.

If apartments are so highly coveted by investors, and if the property fundamentals in that sector are improving, why is the CMBS multifamily delinquency rate so high?

“A lot of the multifamily distress is concentrated among a few very large assets,” says Spencer Hollerith, a research analyst with Trepp.

For example, a whopping $3 billion CMBS loan on Peter Cooper Village/Stuyvesant Town, a 110-building residential complex in Manhattan, was taken back by special servicer CW Capital in 2010. The owners ran intro problems when they tried to convert rent-stabilized residences into rental units.

“The top 10 largest delinquent multifamily loans have an outstanding balance of $5.7 billion, just over 37% of the total delinquent multifamily balance,” says Hollerith. “Those alone account for about 630 basis points of the multifamily delinquency rate.”