In several cases over the past few years, the Minnesota Tax Court has found a taxable property value higher than the amounts presented in witness testimony from either side of a tax argument.

Because the Tax Court has the power to increase values as well as decrease them, this trend has raised concerns when considering whether a case should be taken to trial. However, a Minnesota Supreme Court opinion issued this year suggests that the Tax Court’s decisions in the future are more likely to reflect facts presented in testimony.

Legal showdown

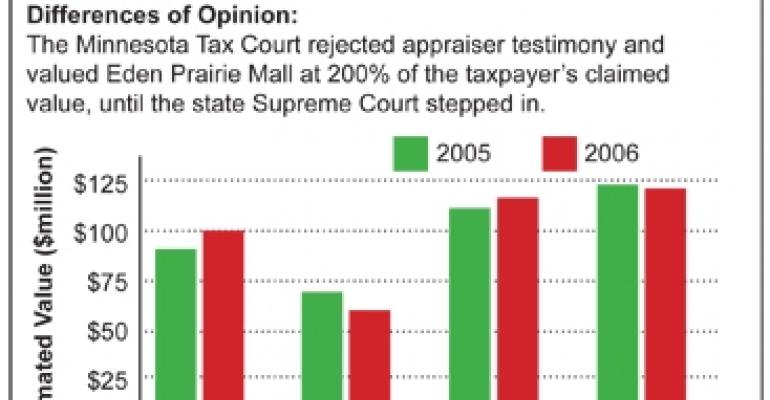

The pivotal decision stems from Eden Prairie Mall, LLC vs. County of Hennepin in which the Minnesota Supreme Court rejected the Tax Court’s value increase for a recently renovated mall from $90 million to $122 million.

The Supreme Court has said the Minnesota Tax Court cannot simply copy a county attorney’s memorandum — including arithmetic mistakes — when deciding to find a value for a property that is higher than that testified to by either appraiser.

Both the taxpayer and government presented appraisals prepared by independent appraisers who had earned the MAI designation from the Appraisal Institute. (The professional accreditation refers to “Member, Appraisal Institute.”)

The diverse appraisal testimony included value opinions for Jan. 2, 2005, and for Jan. 2, 2006, as a separate value must be found for each year in Minnesota.

The taxpayer’s appraiser relied exclusively on an income approach, citing the lack of comparable sales, and testified to a value of $68.75 million in 2005 and a value of $60.55 million in 2006.

The original assessments being appealed put the mall’s market value at $90 million in 2005, increasing to $100 million in 2006. The government’s appraiser gave most weight to the income approach, testifying to a value of $110 million in 2005 and $115 million in 2006. Neither appraiser prepared a discounted cash flow analysis.

The judge based her decision on a direct-capitalization income approach, finding that the government’s cost and sales approaches were not meaningful given the recent major renovation of the mall. The Tax Court found the value of the mall to be $122.9 million the first year and a slightly lower $120.1 million for the later assessment.

In the decision, the Tax Court adopted an argument made by the government’s attorney, which resulted in the indicated value being higher than that found by the government’s appraiser. Like the government’s attorney, the court stated that the government’s appraiser had made a mistake in his calculations.

Independent judgment

The Supreme Court said that the Tax Court did have the authority to make a value determination that is higher or lower than the testimony of the experts because the judges bring their “own expertise and judgment in valuation matters.”

The Supreme Court noted, however, that “market value determinations involve the exercise of complex and sophisticated judgments of market conditions, anticipated future income, and investor expectations ….” In other words, the Tax Court can set taxable values based on its own analysis supported by the factual record. But did that analysis occur?

The Supreme Court pointed out that the Tax Court rejected both appraisers’ opinions of market value and adopted, verbatim, a calculation presented by the government’s attorney in a post-trial brief, “including several arithmetic errors.”

The Supreme Court said “adopting verbatim the recalculated assumptions and nearly verbatim the value determinations … presented in a post-trial brief raises doubts over whether the Tax Court exercised its own skill and independent judgment.”

Although the Supreme Court affirmed other portions of the case, including the increase in value of a separate anchor store, this part of the case was returned to the Tax Court for additional explanation, including its use of income higher than that used by either appraiser.

Furthermore, the Supreme Court explicitly stated the Tax Court could reopen the record and admit additional evidence. It is not clear whether the Tax Court must admit additional evidence, but presumably the taxpayer will seek to do so when the Tax Court reconsiders its decision. At this writing, the Tax Court has not issued a new decision.

It is now clear that the Minnesota Tax Court doesn’t need to merely pick one of the taxable property values presented at trial and can find a taxable value outside the range of values introduced at trial.

Importantly, however, it is also clear that the Minnesota Supreme Court will scrutinize those findings, demanding that the Tax Court explain in detail why it is rejecting the testimony and substituting its own opinions and data.

This precedent-setting case could encourage the Tax Court to stay within the range of testimony from the various appraisers, absent a compelling explanation for doing otherwise.

John Gendler is a partner in the Minneapolis law firm of Smith, Gendler, Shiell, Sheff, Ford & Maher, P.A., the Minnesota member of American Property Tax Counsel, the national affiliation of property tax attorneys. He can be reached at [email protected]