Capital is pouring back into the commercial real estate market, giving lenders and borrowers something to celebrate. Yet a volatile economic recovery, looming interest rate hikes and pending legislative changes are just a few of the issues putting a damper on that enthusiasm.

“There is a ton more activity in the marketplace, and the slope of activity has increased very positively over the last year,” says Jack Cohen, CEO of Chicago-based Cohen Financial.

The total volume of U.S. commercial and multifamily originations reached $118.8 billion in 2010, a 44% increase compared with the $82.3 billion that occurred as the market hit bottom in 2009, according to the Mortgage Bankers Association (MBA).

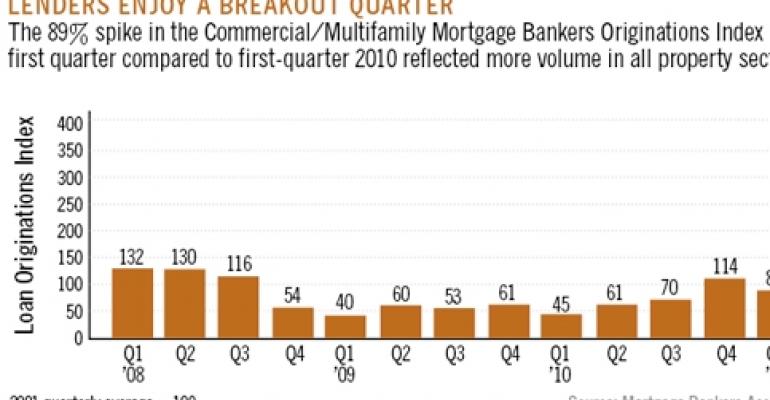

In addition, loan origination volume jumped another 89% during the first three months of 2011 compared with the same period a year ago, according to the MBA's first-quarter survey (see chart).

The return of the commercial mortgage-backed securities (CMBS) market has certainly played an important role in that improved liquidity. CMBS issuance through the first five months of 2011 totaled $12.6 billion, already surpassing the $11.6 billion that was recorded in all of 2010, according to industry newsletter Commercial Mortgage Alert.

Industry experts expect that CMBS issuance will reach between $35 billion and $50 billion this year.

“Every single day the box gets a little bit bigger, and the markets get a little bit bigger relative to what the lenders will finance,” says John Pelusi, executive managing director and managing member of Houston-based HFF LP.

Life insurance companies started out at the beginning of 2010 offering 50% to 55% loan-to-value. That ratio has gradually crept higher to the current rate of 75% loan-to-value for best-in-class borrowers and properties.

“You've also seen an increase in the amount of mezzanine and preferred equity available to help capitalize projects,” adds Pelusi.

However, it is also important to put that rebound into context. “We as an industry have a new normal, and the shrinking and comparison of stats is somewhat misleading,” says Cohen.

Lending activity is still well off the pace of 2005 and 2006 when originations were at or above $400 billion per year. The $118.8 billion in commercial and multifamily loans originated in 2010 is less than half the $263 billion in loans that closed in 2004, according to the MBA.

Aversion to risk remains

Lending activity is continuing to be fueled by an appetite for trophy properties. There is a lot of capital, almost bidding wars, for best-in class properties in top markets. In contrast, there is almost no capital for troubled properties.

“The dominant trend is that the market still has no idea how to identify, assess and price risk, but rather they are pricing based on scarcity value,” says Cohen.

Capital is flowing freely to trophy assets in top markets such as New York, Washington, D.C. and Los Angeles. “During the last 12 to 15 months, that has only been further emphasized. We see an abundance of capital looking for those kinds of assets in those markets,” says Pelusi.

Intense competition for those top assets is prompting both debt and equity to expand to Class-A properties outside of top-tier cities into smaller metros such as a Dallas, Seattle or Miami.

It is no wonder that lenders remain wary of risk. The housing crisis continues to drag down the economic recovery. The industry also is facing monumental changes related to the Dodd-Frank Wall Street Reform and Consumer Protection Act, as well as expected reforms to Fannie Mae and Freddie Mac.

As the economy and the commercial real estate market continue to recover, lenders are adapting to the “new normal” and are trying to get comfortable with the many risks that remain in the market.

“By and large everyone's view is that we as an economy and we as an industry have turned the corner,” says Cohen, “and we will continue to make progress.”

CLICK BELOW TO SEE: