Prices for real estate, like any other economic good, are a function of supply and demand. Since each market has different underlying demand drivers and supply constraint characteristics, investment returns vary.

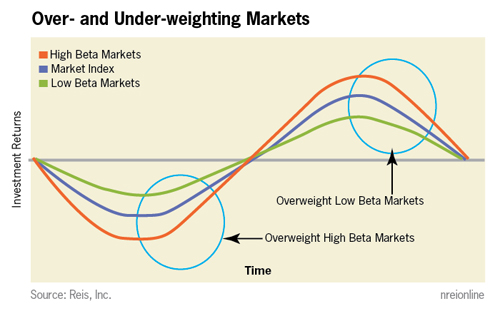

Compared to the indices such as NCREIF Property Index (NPI), returns for some markets are historically more volatile than others. Market volatility, defined as beta (β), is not necessarily a negative feature as markets with higher volatility often out-perform during the recovery phase of the real estate cycle. Usually however, high beta qualities are associated with higher risk as like leverage; this characteristic can accentuate a market decline. Overweighting high beta property sectors and markets during the current real estate recovery may be a way to enhance returns.

Risk beta

The total risk of a portfolio is comprised of market risk and asset specific risk. Asset specific risk can be diversified away while market risk cannot. Market risk is commonly measured as beta (β). Beta is a quantitative measure of the volatility of a market, a property sector, or a portfolio relative to a broad market index. For instance, market beta is defined as:

Generally speaking, a beta of 1.0 indicates that the market’s returns move in line with the broad market index. A beta of 1.2 means that the asset’s return is likely 20 percent more volatile than the broad market index return, while a beta of 0.8 means that the asset’s return is 20 percent less volatile than the broad market index return.

Property sector beta

Property sectors have different betas. As might be expected, the hotel sector has the highest beta and is typically considered the riskiest property type. This makes sense because hotels rely on daily room rentals. Therefore, hotel performance tends to suffer immediately and dramatically during economic downturns, but generally recovers more quickly with the economy and often the highest returning sector in a cyclical upswing as we have seen over the last three years. Historically, demand for office space is especially sensitive to economic conditions and employers have the tendency to over-fire and over-hire office workers through the cycle. The apartment sector has a beta slightly lower than average, as relatively steady demand for rental housing has typically made it less sensitive to the economic environment than the other sectors. The retail sector, supported by resilient consumer spending and longer leases, has the lowest beta among the five property sectors.

Market beta

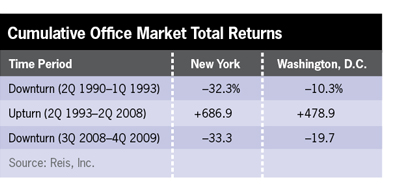

Typically, a market with a higher beta relative to the NPI index tends to have higher returns when the index is increasing and lower returns when the index is decreasing. For example, New York tends to have a higher beta than Washington, D.C. over several market cycles.

Concentrated in financial services, the New York office market has shown greater volatility than the D.C. office market, which is much more diversified and includes a high concentration of employment in less economically volatile sectors such as government, health care, education, and the defense industry. Consequently, total returns for the New York office market are much lower than the D.C. office market during the last two downturns, but significantly higher during the upturn. A simple comparison of returns below shows this.

Beta investment strategy

Understanding market beta behavior may be useful in identifying opportunistic markets as well as in managing portfolio risk. An investment strategy focused on beta would seek higher returns by timing the real estate market cycle and taking on calculated market risk, with the goal of outperforming the market benchmark NPI index. The strategy requires a thorough understanding of market fundamentals and an estimate of future market performance. In the early part of an upturn cycle, it is desirable to overweight high beta sectors/markets to maximize portfolio returns. As the market moves towards a peak, the portfolio would shift to overweight low beta sectors/markets, in order to minimize potential losses during a downturn.

As the economy and capital markets continue to improve, we believe that a portfolio that is overweighted in high-beta sectors and markets is likely to out-perform the benchmark NPI index over the next few years.

Of course, a portfolio with higher beta will inherently have higher risk, which could negatively impact portfolio returns during a market downturn.

David Lynn, Ph.D., serves as Chief Investment Strategist at Cole Real Estate Investments, Inc. The views and opinions expressed in this commentary are those of the contributor as of the date of publication and are subject to change, and do not necessarily reflect the views of Cole Real Estate Investments and/or its affiliates.