With nonfarm payroll employment rising across the United States by 290,000 in April, and with more than 570,000 jobs added nationwide in 2010, Atlanta is following suit with consecutive months of new net job growth of its own. The capital of the southeast added approximately 4,500 jobs in February and 10,000 jobs in March. So, why does the Atlanta office market still sit at a vacancy rate of 22.6%, according to Grubb & Ellis? Industry analysts say be patient, a turnaround is afoot.

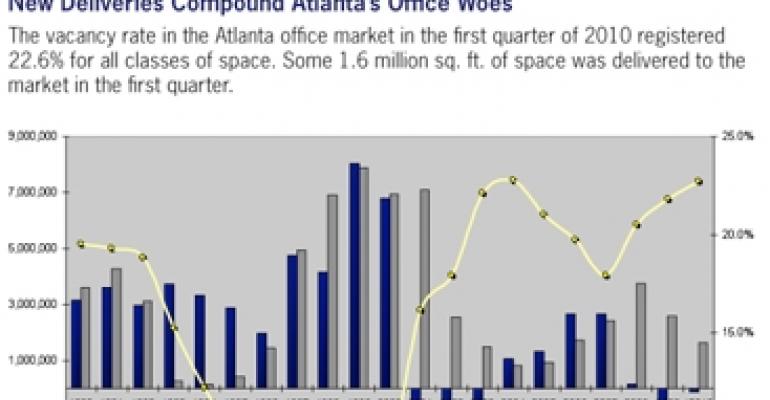

The first quarter of 2010 brought an uptick in leasing and the market’s first positive absorption, although modest, since 2008. However, with the delivery of three new office buildings totaling 1.6 million sq. ft. of vacant space in the first quarter — Phipps Tower and 3630 Peachtree in Buckhead, and 1075 Peachtree in Midtown — overall vacancy rates continued to rise despite the positive absorption numbers.

Buckhead and Midtown’s new towers, though, are the last in Atlanta’s office development pipeline for sometime. “It might be five years before we see the next possible spec building,” says Scott Amoson, director of research for Colliers International.

As financing for new development continues to be a tough sell, Amoson says developers will have to bring a significant amount of pre-leasing agreements to the table before any development is even considered in Atlanta.

“There are no office cranes in Atlanta today, and that’s good,” says Brett Hunsaker, executive vice president with brokerage firm Grubb & Ellis. “I think we needed a rest from the cranes.”

Still, Hunsaker remains bullish on the Atlanta office market. “There’s much more activity on our listings, more calls from brokers, tenant representatives showing more space, so optimism is high,” Hunsaker says. “The caution is making sure we solidify what we need to in absorption and then begin to look toward future development.”

The slowing pace of development should allow for Atlanta’s office vacancy rates to stabilize through positive absorption in 2010, reaching a natural balance of supply and demand. After Atlanta posted negative absorption of 1.8 million sq. ft. in 2009, according to Colliers International, and with a record amount of available office space in the market, the recovery is expected by many to be slow but steady.

Atlanta and its metro area continue to attract new corporate headquarters away from northern cities like NCR’s recent move from Dayton, Ohio, to Duluth, Ga. First Data Corp. and Sony Ericsson are also relocating their headquarters to Atlanta. New corporate headquarters mean more jobs for Atlanta, and more jobs mean more absorption of office space.

According to Dan Wagner, research manager of Grubb & Ellis, one office job equals 151 sq. ft. of absorbed office space in metro Atlanta. To reach a vacancy rate of even just 15%, though, Atlanta would need to absorb more than 10 million sq. ft. of office space, requiring the addition of 70,000 new office jobs.

“Slower growth is atypical of Atlanta’s office market, but it may stave off another absorption bubble similar to those that appeared prior to the previous two downturns,” Wagner says. “Ultimately, the key to office market recovery lies in Atlanta’s ability to attract and retain jobs.”

And when the market recovers, developers will come back. “When office space drops to an 18- to 24-month supply period, you’ll see cranes back in Atlanta,” Hunsaker says. “Developers will see the opportunity to get back into the game.”