Concerns about financing and a sluggish U.S. economy won’t deter commercial real estate investors.

Despite a softening economy and turmoil in the capital markets, investors continue to have confidence in the U.S. commercial real estate industry. A survey of more than 1,000 private and institutional real estate investors shows only one in five respondents believe the economy will be stronger in 2008, yet the majority want to invest more funds in the sector.

“To see that a majority of investors are still planning to increase real estate holdings and that the percentage is higher than last year is a strong validation that they are separating capital markets issues from commercial real estate fundamentals,” says Harvey Green, president and CEO of Marcus& Millichap Real Estate Investment Services.

The survey, dubbed the 2008 Real Estate Investor Outlook, was conducted jointly by National Real Estate Investor, Marcus & Millichap and Countrywide Commercial. This is the fifth year in a row this exclusive survey has been administered to U.S. real estate investors.

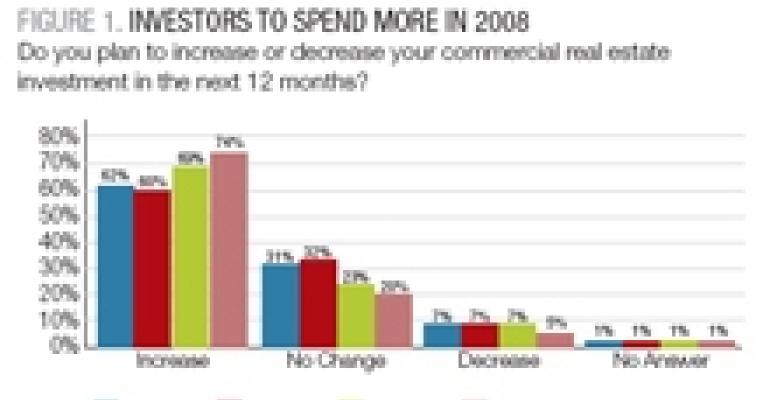

The survey reveals that 62 percent of respondents plan to increase allocations in real estate over the next 12 months compared to 60 percent in 2006, 69 percent in 2005 and 74 percent in 2004. Only 7 percent of real estate investors plan to decrease their investments in real estate over the next 12 months (see figure 1).

“Investors are going to invest more in real estate because pricing is more attractive and they’ll be able to get slightly higher yields,” says Chris Tokarski, managing director of Countrywide Commercial’s real estate finance group. Of the investors who plan to increase their real estate holdings, the average estimated increase is 21 percent.

“Availability and cost of debt may have changed, but healthy occupancies, rent growth, lack of overbuilding and moderation in prices are the drivers behind the optimism,” adds Green.

Investment sales activity in 2007 is on pace to eclipse 2006’s $356 billion, according to Real Capital Analytics Inc. As of October 1, the New York-based research firm, which tracks all deals $5 million and above, had recorded $356 billion in sales of the five main property types (office, apartment, retail, industrial and hotel).

For the first two quarters of 2007, U.S. commercial property provided a cumulative return of 8.21 percent and is on track to at least meet the 2006 annual return of 16.6 percent, according to the National Council of Real Estate Investment Fiduciaries.

“People who have invested in real estate over the past several years have enjoyed really good returns,” says Rick Cavenaugh, president and COO of Fifield Cos., a Chicago-based developer and owner that specializes in multifamily and office properties.

“We believe there will still be ample capital flowing into the real estate sector because returns will still be pretty strong, even as they come off the levels where they were.”

In order to gain an in-depth understanding of investor attitudes and expectations about the commercial real estate industry, NREI, Marcus & Millichap and Countrywide Commercial collected data from August 16 to September 17, 2007. Similar to previous years, private investors account for the largest group of survey participants (45 percent). This year’s survey also questioned a large number of developers – roughly 13 percent of overall respondents. The survey also includes the views of 92 institutional investors.

Respondents have an average of 19 years’ experience in the industry and an average of $36.6 million invested in real estate. On average, 62 percent of respondents’ portfolios are allocated to real estate.

Among the key findings:

• Only 16 percent of respondents predict the economy will be stronger in 2008 than it was in 2007. Another 41 percent expect the economy will stay the same, while 42 percent expect it will be weaker. When compared to respondent responses from previous years, this survey indicates concerns about the economy have grown significantly since 2004 when 63 percent expected the economy to be stronger over the next 12 months and only eight percent expected it to be weaker (see figure 2).

• Availability and cost of financing moved up to the top concern for 2008. Unforeseen shocks to the economy rank as the second-highest concern among all groups except developers; 43 percent of developers express concern over rising interest rates (see figure 3, page 4).

• Investors are optimistic about rental increases, although not as much as they’ve been in the past. Seventy-eight percent of respondents expect to see an increase in effective rents for one or more property types compared to 84 percent in 2006. Investors feel most positive about rental increases in the apartment sector.

• Replacement cost continues to be a key criterion for investors when they make acquisitions. Almost 90 percent of investors agree that replacement value is important. Nearly two-thirds of respondents indicate their most recent acquisition was at or below replacement cost, while 12 percent of respondents say their acquisitions were above replacement costs.

• Sixty-one percent of respondents say that returns are artificially low, with 38 percent predicting that returns will rise back to long-term averages as conditions change and 23 percent forecasting returns will rise as conditions change but will not reach long-term average levels.

HOUSING HURTS

John Donne’s famous quote ““No man is an island” definitely applies to the commercial real estate industry. Despite the industry’s insistence that the troubles in the residential real estate market had absolutely nothing to do with it, the commercial real estate sector has suffered.

“The commercial real estate industry has caught a cold from all the coughing and sneezing of the housing market, which is deathly ill,” notes Dennis Yeskey, national director of Deloitte & Touche LLP’s Real Estate Capital Markets Group.

Although everyone had high hopes the U.S. housing market would have a soft landing, increased foreclosures and the meltdown in the residential mortgage market caused the housing sector to crash-land. Even worse, the residential mortgage crisis spread to the rest of the credit markets, infecting everything from corporate bonds to commercial mortgagebacked securities (CMBS).

Most survey respondents believe the housing market will be unstable for at least 12 more months. In fact, only 14 percent of investors say the housing market will stabilize within the next few months.

Housing starts fell 2.6 percent in August to 1.3 million as the downswing in the housing market continued, according to the U.S. Commerce Department. Starts were down 19.1 percent from a year earlier, falling to the lowest level in 12 years. In August, existing inventory reached the highest level since February 1988 with an inventory-sales ratio of 9.8 months, according to the Mortgage Bankers Association (MBA).

Dennis Lockhart, president of the Federal Reserve Bank of Atlanta, believes that the bottom of the housing downturn could arrive during the second half of 2008 or even later.

That’s not good news for the U.S. economy, especially when you consider that prior to the recent downturn in housing, there were 10 prior housing declines during the postwar period and all but two of them were followed by a recession. (The exceptions were the housing declines in 1950 and 1966 when major increases in defense spending helped keep the economy afloat.)

In fact, the outlook for U.S. growth has deteriorated due to the weak housing market and increasing concerns of defaults on subprime mortgages. RREEF Research is forecasting economic growth of just 1.8 percent in 2007, and 2.2 percent in 2008 compared to 2.9 percent in 2006 and 3.1 percent in 2005. Consumer spending is expected to drop from 2.8 percent this year to 2.3 percent in 2008, and unemployment is expected to rise from 4.6 percent to 5.1 percent.

“There is no doubt that the economy is more vulnerable to any additional disruptions after the credit-tightening that has occurred,” says Hessam Nadji, senior vice president and managing director of Marcus & Millichap Research Services. “We don’t believe the housing downturn has bottomed, and that will be a drag on the economy

well into 2008. However, strength elsewhere, particularly corporate balance sheets, profits, business investments and exports should result in a slowdown rather than a recession.”

FINANCING WORRIES

Still, there are ongoing concerns about the credit markets for both residential and commercial real estate. In fact, availability of financing is the top concern for respondents in this year’s survey. Last year, only 16 percent of respondents were worried about it – more were concerned about the economy and cost of building materials.

Six out of 10 respondents say debt financing will be harder to get over the next 12 months, which compares to just 35 percent in 2006 (see figure 4). And they have every right to be spooked by what’s happened in the capital markets.

“There’s a global liquidity crisis in all asset classes that is going to make financing much more difficult,” Tokarski says.

In mid-summer, the CMBS market all but shut down as bond buyers exited the market, leaving billions of dollars’ worth of CMBS paper in “warehouses” and forcing many borrowers to pursue debt financing from portfolio lenders including life insurance companies. At their worst, CMBS spreads had widened to swaps plus 70 basis points for 10-year triple-A bonds, while triple-B- spreads widened to swaps plus 425 basis points.

“I would describe the capital markets’ adjustment to commercial real estate as an overreaction to the residential subprime issue,” Green says, adding that he expects the capital markets to settle down and spreads to decline eventually. “But they will not go back to their pre-July 2007 conditions.”

Before the subprime meltdown and subsequent credit crisis, $136.7 billion of CMBS loans were originated during the first half of 2007, an increase of 55 percent from the same period in 2006, according to MBA.

As of early October, CMBS lenders were still working through much of the warehoused paper. But only $10 billion worth of CMBS bonds were priced in September, less than half of the $26 billion that was initially projected, according to RBS Greenwich

Capital, one of the world’s largest CMBS issuers.

Many of the deals that were slated for September were expected to come to market in October, pushing projected issuance to $34.2 billion. If no other deals come to market in 2007, domestic issuance will total $245.4 billion, or 21 percent above 2006’s total, according to RBS Greenwich Capital. The firm initially projected 2007 issuance at $290 billion.

Fortunately, there are signs that the CMBS market is calming down. Fixed-rate CMBS spreads tightened in early October, with triple-A spreads reaching swaps plus 55 basis points. The tightened spreads, along with lower interest rates, mean investors’ cost of debt has decreased.

“By the beginning of the second quarter 2008, I think the upheaval in the credit markets will work its way out, but the stricter underwriting will be here to stay,” says R. Craig Butchenhart, president of NorthMarq Capital Inc., one of the largest mortgage banking firms in the nation.

In fact, underwriting standards today are much more conservative than they were in 2006 and early 2007. Ratings agencies Fitch Ratings and Moody’s Investors Service both issued reports earlier this year indicating that conduit lenders had become too aggressive in their underwriting and loan terms, putting CMBS investors at risk.

“Over the last five years, anyone who could breathe could get a loan and could buy real estate,” Tokarski says, adding that investors are going to have a much harder time raising debt and equity in today’s market.

Previously, many loans were based on projected income streams rather than current income streams. Borrowers routinely closed highly leveraged loans, with loan-to-value ratios exceeding 80 percent. Moreover, interest-only loans (IO) were easy to come by, with many borrowers obtaining 10-year IOs.

Today, loan-to-values have returned to more traditional levels in the 70 percent range, while IO provisions have all but disappeared. “This was a muchneeded adjustment that will make our industry much stronger,” says Scott Derrick, chief acquisitions officer of SCI Real Estate Investments, a Los Angeles- based tenant-in-common (TIC) sponsor that is scheduled to make roughly $550 million in acquisitions this year.

The stricter underwriting standards and lower leverage limits are good news for SCI Investments and other investors with long track records that aren’t overly debt-dependent. “If you can find the right deals and can align yourself with financing, it can be

a good opportunity to invest,” says William Hughes, senior vice president of Marcus &

Millichap Capital Corp. “It’s a better environment for sophisticated investors because lenders are going to back borrowers with more experience and a longer track record.”

FROTHINESS FADES

The challenging debt markets and tighter underwriting standards are expected to impact asset pricing and cap rates.

“We’ve seen the highly leveraged buyers leave the market because they haven’t been able to close loans,” Derrick says. “That means there’s less competition and less pressure on pricing.” In fact, SCI hopes to invest $700 million in real estate in 2008.

San Diego-based office and industrial investor Equastone also has high hopes for 2008 and is targeting a total investment of $1 billion, says chief investment officer Jeff Schindler. The firm had similar goals for 2007 but is “proceeding with caution” to make sure its acquisitions are priced appropriately. “Since the highly leveraged buyers have been sidelined, the market has lost some of its frothiness,” he explains. “There’s still some NOI growth that supports strong pricing, but there aren’t as many buyers showing up.”

While respondents are split on whether pricing for commercial property has reached a peak – 44 percent of respondents say yes and another 36 percent say no – most do anticipate a decrease in pricing for most property types (see figure 5).

That response is a big change from last year’s survey when the majority of respondents expected pricing to increase for all property types except for grocery-anchored retail and regional malls (see figure 6).

“I think we are entering a period of realignment between the rate of price appreciation and rent growth, but to say we have peaked implies prices across the board will stagnate or fall, and I do not believe that will be the case because of healthy fundamentals,” Green says.

In fact, Green expects rents to continue to grow across most property types, although the pace will be slower than it has been for the past several years. “The recovery period is behind us for office, apartments, industrial and hospitality, creating a more normalized market rather than a recovering market in which vacancies have a long way to drop and rents have a long way to climb. Retail, which never had a downturn, is now more likely to experience slower rent growth because of weakness in housing,” he explains.

Additionally, the slowing economy will reduce the pace of absorption, and in some markets – such as those that are vulnerable to financial services or mortgage industry cutbacks – vacancies will rise and rent growth will stall, at least temporarily.

“It all depends on the economy, and if the economy slows, we won’t see any rent growth,” Yeskey says. “But we won’t see any decreases either.” The majority of respondents agree – four out of five do not expect a decrease in the effective rents for any property type. In fact, 78 percent of respondents expect to see an increase in effective rents for one or more property types with apartments leading the way (see figure 7).

In addition to healthy fundamentals, commercial property valuations are well-supported by replacement costs. “It still costs far more to build a building than it does to buy an existing one, not to mention the difficult approval process in most markets,”

Nadji points out. “Replacement cost is still well above acquisition pricing in most markets and property types.”

And although construction costs may not be increasing at the rapid pace they were six to eight months ago, they’re still high enough to make development more difficult than acquisition.

“I expect there is going to be less development in 2008 because construction financing is much more difficult to get,” Tokarski says. “If a project is not already under way, I doubt it will break ground without pre-leasing.”

Last year, construction costs were one of the top three concerns for survey participants. This year, worries about construction costs were less acute. However, seven out of 10 respondents experienced an increase in construction costs over the past 12 months, and more than half expect an increase in the next 12 months. The survey suggests that construction costs increased an average of 16 percent. Going forward, respondents forecast construction costs to increase six percent.

Many experts say the slowdown in single-family housing construction has decreased demand for commonly used building materials, therefore mitigating extreme price increases. However, construction costs continue to be a big concern for Chicago-based Fifield Cos., which develops high-rise apartments and office buildings.

“Demand for concrete and steel hasn’t dropped off because there are still a lot of projects under development that use these materials – particularly public projects,” Cavenaugh says, adding that global demand for these building products continues to be high as well.

All of these market dynamics make a substantial price correction unlikely. In fact, only eight percent of respondents expect a major pricing correction, while 90 percent expect there to be a minor or modest pricing correction for commercial real estate assets.

Tokarski forecasts a five percent to 10 percent decrease in pricing for top-tier real estate and a 10 percent to 15 percent decrease for assets in secondary and tertiary markets. If the market does experience a 10 percent pricing correction, that 10 percent corresponds directly to the appreciation commercial property experienced from fourth quarter 2006 through first quarter 2007 when underwriting was at its most aggressive.

“Many buyers have become more cautious – as have lenders – and there is much more focus on real income as opposed to aggressive pro forma expectations,” Green explains. He, too, expects buyer demand and pricing for higher-quality assets in primary markets will remain strong, while lower-quality assets will see more of an adjustment, especially in secondary and tertiary markets.

Respondents expect cap rates to increase for all property types over the next 12 months, but the increase is expected to be slight – only 29 basis points. As of early October, the average cap rate for commercial property was 6.94 percent, according to Real Capital Analytics. In 2006, the average cap rate was 7.12 percent.

The upward pressure on cap rates comes from the credit crunch and the looming threat of recession, Nadji says, adding that cap rates for top-tier properties are not expected to rise more than 25 basis points while cap rates for lower-tiered properties and markets will increase 50 basis points to 75 basis points.

Bob Dougherty, chief acquisitions officer with Buchanan Street Partners, has already seen a 25-basis-point increase in cap rates. “Many cap rates have been predicated on the availability of cheap debt, and that’s driven pricing to artificially high levels,” he notes. “We’ve been underwriting a 100-basis-point increase in cap rates for almost two years because we’ve been expecting a correction. Now we think cap rates will return to historical norms of 200 [basis points] to 300 basis points over Treasuries.”

But NorthMarq’s Butchenhart is less confident that returns will ever return to historic levels. “Real estate is recognized as a strong asset class by most investors today, so returns are not going to go back to where they were when investors didn’t recognize the asset class,” he says.

APARTMENT APPEAL

Apartments and mixed-use assets are the most attractive to respondents. In fact, 33 percent of them say they’ll enter the apartment sector in the next 12 months, and 19 percent indicate they’ll enter or expand into the mixed-use sector. Office properties and retail assets rank far lower with investors, according to the survey.

Investors are increasingly interested in the apartment sector. In 2004, for example, roughly $51 billion worth of apartment assets changed hands in the U.S. – about $1 billion less than the volume of transactions during the first three quarters of 2007, according to Real Capital Analytics.

Today, much of the investor interest in apartments is driven by the weakness in the housing sector and continued upheaval in the mortgage markets. “With both the condo market and the single-family home market falling apart, people have to live somewhere, so they’re going to rent apartments,” Yeskey points out.

Buchanan Street Partners is bullish on the apartment sector, Dougherty says, and plans to grow its portfolio by investing in the multifamily sector. “We like the demographic and demand trends in the sector because affordability of single-family housing is out of reach of many people,” he explains. This year, the company is on track to close $325 million to $350 million in new equity investments. Next year, it is shooting for $400 million to $450 million.

Dougherty, along with many other investors, expects apartments to benefit from increased pricing and rental rates. In fact, three out of four respondents who are currently invested in apartment properties predict an increase in effective rents, and nearly one-third expect to see an increase in the market pricing of apartment properties. More than half of those who invest in apartments expect a slight or major increase in cap rates.

As of October, the average cap rate for apartment properties was six percent and the average price per unit was $104,857, according to Real Capital Analytics. To compare, the average cap rate in 2004 was 8.66 percent and the average price per unit was $67,776.

Alan George, chief investment officer for Equity Residential, says cap rates for Class B and C apartment properties have increased 25 basis points and 75 basis points, respectively, since mid-summer. “I think cap rates for those types of assets has plateaued, and I wouldn’t expect more of an increase in 2008,” he notes, adding that Class A cap rates have moved very little.

Some industry experts are less enamored of apartments. Yeskey, for example, feels apartment cap rates are too low for most investors to make a good return. “I really worry about the cap rates on apartments – investors better be sophisticated operators because there’s not a lot of juice there,” he says.

Beyond apartments, Nadji says there are investment opportunities in office and retail. “The office market still has a lot of room to run, and the concerns about the retail sector are overstated,” he contends.

Nadji points out that the office leases that were signed from 2002 to 2004 were at the bottom of the market. “When tenants renew in the future, there is a mark to market that should result in higher rental rates and revenue increases,” he explains. Three in five downtown office investors expect effective rents to increase, and nearly half of suburban office investors expect rents to increase. These numbers are consistent with the 2006 findings.

As for the retail sector, Nadji admits that that there are some valid concerns about consumer spending, which has dropped off significantly this year. But he contends that retail sales are still growing and retail fundamentals are still strong. Most projects that are under development are preleased, preventing serious overbuilding in most markets and keeping the expected rise in retail vacancies moderate.

Property types aside, Nadji expects continued investor interest in properties that they can renovate, redevelop or expand. Nearly half of respondents (45 percent) plan to acquire properties specifically for redevelopment, renovation or expansion. More than two-thirds of developer respondents (70 percent) plan to acquire properties for this purpose. SCI, for example, is raising a $50 million fund specifically to invest in value-added properties in infill locations.

“In a low-yield environment, it is not surprising to see the appetite for value-add investments, but these types of assets will be harder to finance because of the risk level,” Nadji says. “For investors with cash and a higher tolerance of risk, value-added properties will present a great opportunity.”

George agrees: “I think the value-added sector is a more difficult business today than it has been in the past, but rehabs of quality assets in quality locations always make sense.”

View full PDF of the 2008 Real Estate Investment Outlook