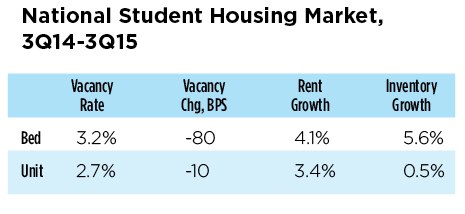

Fundamentals in the student housing sector advanced at a healthy pace during the 2014-2015 school year, mirroring the performance of the greater multifamily sector. Student housing is categorized by buildings leased on a per-unit basis and those leased on a per-bed basis. Facilities that lease by the unit exhibited rent growth of 3.4 percent between the third quarter of 2014 and the third quarter of 2015. Rent in per-bed facilities advanced by 4.1 percent over the same period. Both subtypes exhibited vacancy compression over the year despite already tight vacancy levels: bed vacancies fell 80 basis points to 3.2 percent, and unit vacancies fell 10 basis points to 2.7 percent. For comparison, the national multifamily vacancy rate currently sits at 4.3 percent.

Amenities a plenty

With a lower vacancy rate that looks to be continuing downward, one cannot help but wonder: why has rent growth for the unit-lease subtype underperformed its higher-vacancy counterpart? The answer is found in the substantial new supply of relatively high-end per-bed facilities that came on-line over the past year. Bed inventory increased by 5.6 percent for student housing in the U.S., compared to a meager 0.5 percent increase in per-unit inventory. These per-bed facilities are specifically designed to attract the younger college students; as such, new projects that have come on-line are stocked with amenities foreign to most typical multifamily housing structures.

Consider the HERE Champaign Student Housing Facility in Champaign, Ill. Completed in 2015, the facility caters to students enrolled in the University of Illinois. Tenants leasing beds in HERE Champaign have access to, among a host of other amenities, a sauna, tanning beds, a movie theater, a golf simulator and a yoga studio. This new premium space representing a not unsubstantial portion of overall inventory has helped drive rent growth for the subtype in this market.

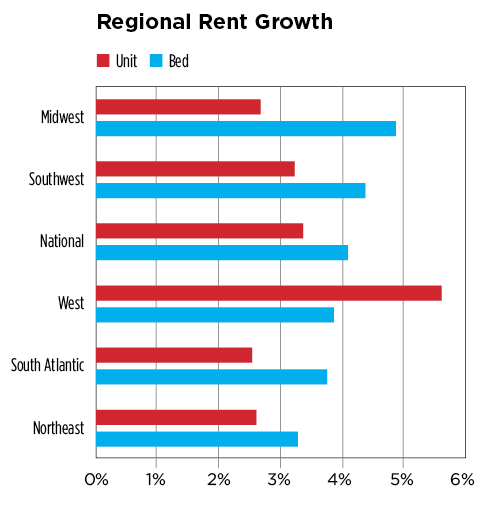

The trend is even more apparent when examining data at the regional level. Regions where inventory of per-bed facilities increased the fastest over the past year are also the regions notching the fastest rent growth. Inventory growth in both the Midwest and the Southwest exceeded 7.0 percent over the past year, and these were the only regions where rent growth surpassed 4.0 percent. This is due to the fact that new inventory tends to weigh heavily on the average rent.

Per unit leasing

Given the similar leasing structure, market dynamics in the multifamily sector have a meaningful impact on per-unit student housing, more so than even the per-bed subsector of student housing (especially in large metropolitan areas). Currently at $1,075, rent levels for the unit subsector are roughly in line with the national average effective rent level for apartments. Again, examining regional data, there is a consistent divide between rent growth in the per-bed subtype and the per-unit subtype. The Midwest notched the strongest per-bed rent growth over the past year, at 4.9 percent, however per-unit rent registered a relatively tepid 2.7 percent increase. The West had the highest unit rent growth of 5.6 percent, but rents in per-bed student housing facilities increased by only 3.9 percent.

Incidentally, the West is the region where one would expect the strongest student housing rent growth. Metros such as Los Angeles, Oakland, Orange County, Seattle and Phoenix have been buoyed by the booming tech and energy sectors and have seen rent growth accelerate with record increases in recent years. These are also metros containing large portions of the region’s student housing inventory as local schools attract many students drawn to the tech sector. Clearly, these student housing markets are not immune from the general increases in these metro’s cost of living.

Despite the fact that both subtypes are market-rate rentals, it is apparent that per-bed and per-unit facilities are not in as close a competition as one would intuitively expect. Per-bed facilities are purpose built for students. It is unlikely that a non-student potential tenant would be interested in renting a bed versus an apartment. At the same time, students renting in per-unit facilities face competition from non-students whose ability to pay rent is dependent on local economic conditions. As previously noted, the Midwest notched the fastest per-bed rent growth. This was also the region with the most per-bed inventory growth, which as mentioned above weighs heavily on rent growth, and the slowest per-unit rent growth. But this is no surprise. There are no major apartment markets in the Midwest that have seen rents surge in recent quarters.

Outlook

The outlook for the student housing sector is decidedly positive. For per-bed facilities, despite the surge in completions, demand should keep pace, pushing vacancies to the mid-2 percent range in coming years. With a lack of significant new supply in the pipeline, per-unit housing will continue to be primarily influenced by forces in the multifamily market. As such, markets where new apartment supply is expected to outstrip demand could fare worse. However, supply, rather than any faltering in demand, remains the primary risk factor. According to the National Center for Educational Statistics, enrollment in postsecondary degree granting institutions is expected to rise 6.7 percent through 2019, exceeding the 5.6 percent increase from the previous five-year period. This suggests continued steady demand for the sector, and thus continued improvement in student housing fundamentals.