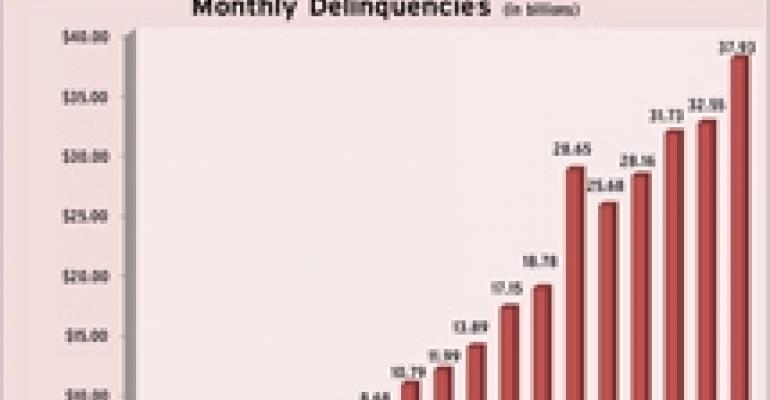

In November 2009, the delinquent unpaid balance for CMBS jumped to $37.93 billion from $32.55 billion a month prior, according to Horsham, Pa.-based Realpoint LLC. It was the second largest one month jump that Realpoint has measured and was driven primarily by the 30-day delinquency status of the $3.5 billion portion of a $4.1 billion Extended Stay Hotel loan.

Overall, the delinquent unpaid balance is up 440 percent from a year ago and is now more than 17 times the low point of $2.21 billion in March 2007. Realpoint noted an increase in each of the five delinquent loan categories in November, while the distressed 90+-day, foreclosure and REO categories grew in aggregate for the 24th straight month. The total unpaid balance for CMBS pools reviewed by Realpoint for the November 2009 remittance was $806.11 billion, down from $810.9 billion in October.

The resultant delinquency ratio for November 2009 of 4.71 percent (up from the 4.01 percent reported for October) is almost six times the 0.83 percent reported in November 2008 and 17 times the Realpoint recorded low point of 0.28 percent in June 2007.

Overall, Realpoint now projects the delinquent unpaid CMBS balance to continue along its current trend and grow to between $50 and $60 billion by mid 2010. The firm now projects the delinquency percentage to grow to between 5 percent and 6 percent through the first quarter of 2010 and potentially surpass 7 percent to 8 percent under more heavily stressed scenarios.

By property type, in November 2009, multifamily loans topped retail loans as the greatest contributor to overall CMBS delinquency, at 1.23 percent of the CMBS universe and 26 percent of total delinquency. Overall, $9.9 billion in multifamily loans are delinquent compared to $9.4 billion in retail loans. Retail had been the highest CMBS default contributor since May. The retail default rate grew slightly to 4.49 percent in November from 4.05 percent in October 2009, up substantially from 0.8 percent one year ago.