Terrible headlines from overseas are weighing down our recovery … again. If we aren’t worried about Greece leaving the Euro (February), we’re worrying about international oil and gas prices (April) or Spanish sovereign default (late April). Now Greece is in the headlines again—and that’s bad news for commercial real estate.

“It certainly increases the risk that we are going to have another fairly unspectacular year,” says Ryan Severino, senior economist for New York-based real estate research firm Reis LLC.

“Fairly unspectacular” seems to be the theme behind the numbers in the first quarter reports from Reis. Our modest recovery will continue to be modest until severe uncertainty ends and strong job growth returns, says Severino.

Retail begins to heal

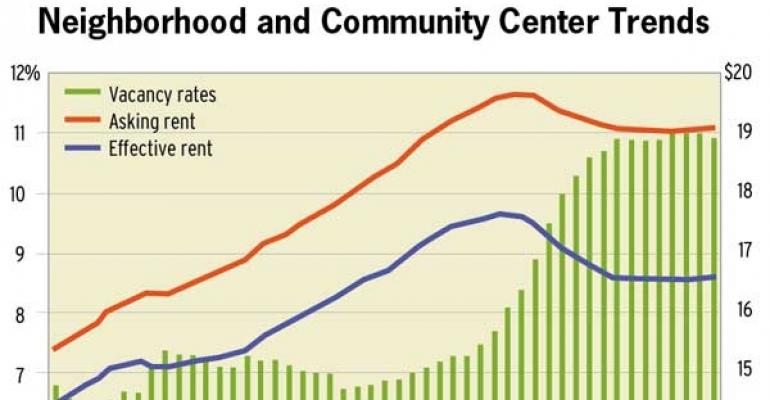

Retail has begun to slowly improve, but the sector is still far from healthy. For example, the vacancy rate for neighborhood and community shopping centers fell for the first time in seven years. Rents also increased, inching up 0.1 percent, continuing the increase in the fourth quarter. “I think we are finally at a point of stabilization,” says Severino. These smaller retail settings have been one of the weakest property types during the crash and its aftermath.

However, effective rents for neighborhood and community shopping centers are still stuck at 2005 levels.

Vacancy rates also improved for regional malls and power centers, falling to 9 percent in the first quarter. The new supply of retail space in malls has been modest — the first new regional mall in the U.S. in six years opened in the first quarter. The small amount of new supply is roughly in line with the small amount of new demand for space.

Overall, the vacancy rate for retail space fell to 10.9 percent from 11.0 percent last quarter. “That’s a welcome change… but it’s just 10 basis points,” says Severino. He says that a healthy vacancy rate for retail space would be below 7 percent.

Slow recovery for office properties

The vacancy rate for office properties has been falling and average rents have been rising since the beginning of 2011. What’s not to like? Quite a bit. The vacancy rate for office space was still 17.2 percent in the first quarter, down only a few basis points of a peak of 17.6 percent. A healthy vacancy rate would be between 12 and 14 percent, said Severino.

He calls the recovery in the market for office properties “tepid.” At least new supply is not a problem. Few new projects opened just before the crash because of high construction costs, and fewer new properties have started construction in the recovery. However, weak supply is matched by weak demand.

“Despite strong profit margins and balance sheets, companies have been reluctant to expand payrolls,” says Severino. Most of the few new jobs so far in this recovery tend to be in other sectors, from the food and beverage business to healthcare.

Nearly all apartment markets strengthen

Not only are apartments markets strong on average—nearly all apartment markets are improving. Effective rents rose in 82 metro areas in the first quarter, according to Reis.

Fairfield County, Conn., is the only metro area in the country where rents fell. But with a vacancy rate of just 4.7 percent, apartments in Fairfield County are hardly in trouble.

On average, apartment vacancies fall below 5 percent in the first quarter in the U.S.—the strongest vacancy rate since late 2001. Our tepid recovery continues to be good for apartments. As long as potential homebuyers hesitate to buy, they will likely continue to rent.

The silver lining

For all of these property types, the markets seem have stabilized. Even in the retail markets, vacancies, occupancies and rents all improved in a majority of the 80 metro areas tracked by Reis.

For real estate investors that means it may no longer be necessary to focus only on the safest, core markets.