Real estate research firm Reis Inc.’s data for the first quarter of 2010 shows that fundamentals at neighborhood and community centers and regional malls continued to slide. And while the pace of declines in occupancies is slowing, rents are still falling at a brisk pace.

Vacancies at both property types rose. For shopping centers, vacancies are at their highest point since 1991 and for regional malls vacancies are at their highest point since Reis began tracking the figure at the end of 1999.

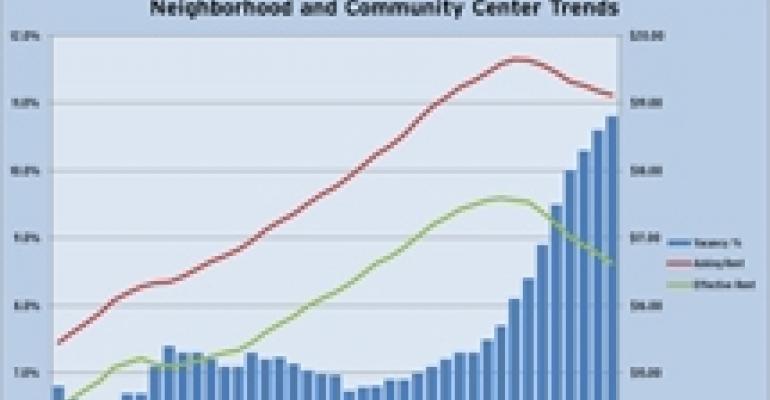

At neighborhood and community centers, the vacancy rate rose to 10.8 percent in the first quarter of 2010. Asking and effective rents continued to decline, falling by 0.3 percent and 0.8 percent respectively. For regional malls, the vacancy rose from 8.8 percent to 8.9 percent. This is the first time in almost 10 years of quarterly history that Reis has observed rent declines for six straight quarters.

The conditions have caused rents to fall to the point where asking and effective rents at neighborhood and community centers are now back to the levels they were in 2005. Asking rents at regional malls have returned to 2006 levels. According to Reis, “We have yet to see a marked deceleration in quarterly rent declines, particularly for effective rents, implying that concession packages are still perceived by landlords as an important tool to attract new tenants and retain existing ones.”

The neighborhood and community center sector posted negative net absorption of 3.0 million square feet during the quarter. That is “progressively less deterioration relative to the quarterly average of 5.6 million square feet that went vacant through 2009.” However, Reis notes that completions have also slowed, with only 865,000 square feet of space coming online during the quarter. In addition, “negative net absorption outstripped the amount of newly completed space for every single quarter from 2009 to the present, indicating that although newly completed buildings contributed some positive amount to occupied space, existing buildings gave up even more occupied stock.”

Overall, Reis maintains a bleak outlook on retail properties. It expects that the slow pace of job growth and inconsistent spending patterns will weigh on retail tenants for another 12 to 18 months. “The retail tenant who plans to expand over the next year and open new stores will be the exception rather than the rule, so Reis continues to project increasing vacancy levels and negative asking and effective rent growth through 2011,” the report says.