In my March column, I indicated that office rents will bottom sooner than expected. Second-quarter results justify this prediction, but it is too soon to pronounce that office fundamentals have bottomed. The latter half of the year will test whether office properties can stage a rebound despite slower economic growth.

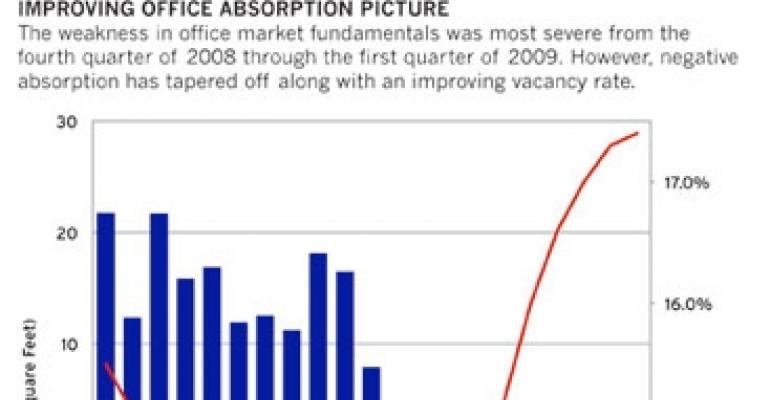

The national office vacancy rate rose by 10 basis points to 17.4% in the second quarter, reaching levels unseen since 1993. Asking and effective rents also fell by 0.2% and 0.8%, respectively. The underlying numbers that make up national figures, however, are shifting toward a more positive outlook.

Vacancy increased in only 49 out of 82 metro markets, down from 60 in the first quarter and 67 in the fourth quarter of 2009. Occupied space declined by 1.4 million sq. ft. across all markets. However, central business districts fared much better, posting positive net absorption of 2.6 million sq. ft.

Some surprises in store

All of this tracks what Reis has forecast over the last six quarters. With favorable supply conditions entering the downturn, office properties are poised to rebound much faster once aggregate demand ramps up.

As we emerge from the downturn, there undoubtedly will be some surprises. We may see asking rents begin to post mild increases even as effective rents continue to slide. Austin, for example, posted a 0.2% increase in asking rent in the first quarter even as effective rents fell by 1.1% and vacancies rose by 60 basis points.

Though these patterns may appear counterintuitive, it is actually quite common to see such results at the inflection point of an economic recovery. It implies positive churn at the property level, with some landlords able to increase asking rents while others need to provide concessions as the battle for tenants continues.

A slower second half

Even as specific markets post encouraging signs of a recovery, national trends will remain muted for the rest of the year. The U.S. economy grew by a moribund 2.4% in the second quarter, consistent with lackluster growth in both the manufacturing and service sectors.

Businesses are gearing up for an eventual recovery, but have started adding to payrolls conservatively and are choosing to invest mainly in capital goods such as equipment and software.

Reis forecasts are consistent with the macroeconomic picture, with generally flat results for the rest of the year. National vacancies will creep up slightly to 17.7% before beginning their descent next year. Rent growth may turn positive by the fourth quarter, but will still finish 2010 below year-end 2009 levels given the declines in the first half.

If office rents do turn positive in the latter half of the year, that will mean eight to nine quarters of declining rents, a far better situation relative to the 14 quarters of negative rent growth from 2001 to 2004.

As prospects for office properties improve, there has been a small sliver of office properties trading at capitalization rates unseen since 2006. Investors are tiptoeing back, but are focusing on stabilized Class-A properties located in primary markets.

Transaction volume comparable to the levels of 2003 and 2004 will probably not materialize until late next year as investors await signs of an economy firmly on track toward recovery.

There is reason to be optimistic about the fate of office properties. A turnaround may yet happen later this year, but the real recovery will come to fruition next year.

Victor Calanog is director of research for New York-based research firm Reis Inc. His monthly column delivers insights on performance trends in commercial real estate.