Under pressure from federal regulators and weighed down by an unhealthy exposure to commercial real estate, small banks — or those in the $10 billion to $100 billion asset range — are making haste to clean up their balance sheets, according to Oakland, Calif.-based Foresight Analytics, a unit of Trepp LLC.

In the fourth quarter alone, the nation’s small banks cut the total outstanding balance of commercial real estate construction and land loans by about 13%, while large banks with assets of $100 billion or more only trimmed back by about 4%, says Matt Anderson, managing director for Foresight.

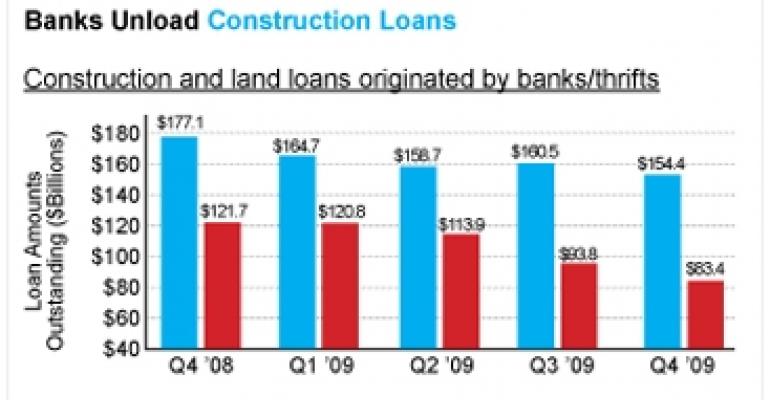

The contrast in the outstanding balance of construction and land loans is even greater when comparing the fourth quarter of 2008 to the fourth quarter of 2009. Small banks held $121.7 billion and $83.4 billion respectively, a 31.5% decline over one year.

“Given that there’s not much in the way of other financing out there right now, to the extent that they’re shedding exposure, it’s more through selling off the loans to someone else or potentially through foreclosures,” says Anderson. The buyers of this debt have generally been private equity players that want to expand into commercial real estate, particularly if there’s a discount involved.

However, Anderson points out that many small banks claim the haircuts on the sales haven’t been as severe as they had originally anticipated.

“Given that the volume of non-performing loans has continued to grow, I’m guessing the ones that are selling are the ones where the bank isn’t having to take as big of a loss,” he says. “They’re choosing which ones to sell and they’re picking the ones that can get somewhat better pricing.”

The loans selected for disposition, in fact, may even be performing loans or “less bad” non-performing loans. For example, the discount on a loan for a piece of land far from an urban center and the discount on a loan for a project already under way in an urban setting is vastly different.

Bad rep

Over the past year, small banks have gained the reputation for not only being over-weighted in construction loans and mortgages but for holding loans of a lower quality than their larger bank brethren.

In February, the Congressional Oversight Panel, established by Congress in 2008 to oversee expenditures of the $700 billion Troubled Asset Relief Program, said that of the approximately 8,100 banks in the U.S., 2,988 are small banks that are dangerously exposed to commercial real estate.

In addition to the lack of diversification, these community and mid-sized banks also hold high concentrations of the riskiest and least sought-after loans, including transition properties and construction loans in secondary or tertiary markets, according to the panel.

The one plus, many small banks contend, is that on the mortgage side of the business they have a significant exposure to owner-occupied properties, which have performed better than income-producing properties. “It’s better but not problem free,” says Anderson.

Owner-occupied properties made up 43% of total loans outstanding for small banks at the end of the fourth quarter, and had a delinquency rate of 4.8%. That compares with 57% of loans backing income-producing properties, which had a delinquency rate of 6% over the same period.

No going back

Despite paring back their commercial real estate exposure, small banks are unlikely to be making room on their balance sheets for new commercial real estate loans. “[They are] cleaning up the risk and not planning on coming back anytime soon,” says Anderson.

With $1.4 trillion in commercial real estate debt maturing over the next five years and no obvious source of funding to soak it up, Anderson does not foresee any major improvement for commercial real estate lending in the near term, even if commercial mortgage-backed securities issuance continues to recover at a healthy pace. “Even if it doesn’t end incredibly badly for everyone, at best [the commercial real estate industry] is essentially treading water.”