As real estate pundits continue to discuss which U.S. cities are best positioned to withstand the economic downturn, Boston ranks near the top of the list. It enjoys some of the highest barriers to entry for retail in the United States.

And, with 4.5 million residents, it's one of the largest urban centers in the country boasting thriving financial, education and health care industries and a reputation as an international destination.

However, much like the rest of New England, Boston proves recessions are not as market-specific as real estate gurus argue.

“The best way to describe it is we are in a period of transition right now,” says Robert Shannon, Boston-based managing director with investment sales brokerage firm Sperry Van Ness/Income Property Realty Advisors. “Even though the prices that are being achieved have not necessarily gone down, there has been a major drop in the number of transactions,” Shannon says.

Over the past year, the city still managed to register the third largest volume of retail investment sales transactions in the United States, with $1.4 billion, after Los Angeles and Chicago, according to New York-based real estate data provider Reis, Inc.

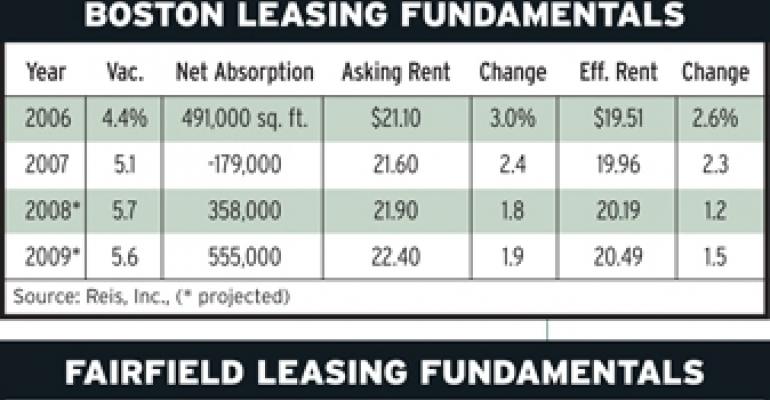

As with much of the Northeast, Boston is better positioned than many other U.S. cities. It recently climbed eight positions to rank No. 10 on Marcus & Millichap Real Estate Investment Brokerage's National Retail Index for 2008. Beantown's asking rents in the first quarter of the year, at $21.60 per square foot, bested the national average by approximately 8 percent, while the 5 percent vacancy rate is less than half the estimated 10 percent projected this year for the nation.

However, the deepening residential housing crisis, exacerbated by the slowdown in consumer spending, has led to less robust leasing and a decline in new construction making investors extremely cautious. “Right now, we are in a bit of a down cycle,” says Nathaniel Heald, an associate with Jones Lang LaSalle, Inc. “But, we will be back.”

Glass houses

A mounting challenge for the New England region is the soft residential sector. In June, Housing Predictor, a Web site that provides real estate market forecasts, ranked Boston as No. 13 on its list of the Top 25 Worst Housing Markets in the Country, forecasting housing prices will fall 11.7 percent in 2008. Across the Charles River, Cambridge, Mass., ranked No. 17 on the list, with its housing prices projected to fall 10.3 percent. And 60 miles south of Boston, New Bedford, Mass., is expected to see an 8.8 percent drop in home values this year.

In the Boston metropolitan area, single-family home transaction volumes have slowed as well — tumbling 33.7 percent from 2007 figures to 1,350 in the first quarter of 2008, according to the Massachusetts Association of Realtors. During the same period, the median sales price slipped 3.7 percent, to $433,250.

“The price is substantially lower than it was 12 months ago,” Shannon notes. “When you think about where the prices were five years ago the market is still healthy; but that's why people get nervous. They are looking at 2007, instead of five, six, seven years ago.”

Sales, rents slip

The rising numbers of foreclosures and the lackluster economy are eroding Bostonians' purchasing power and intensifying the pressure on the city's retail sector. While inventory and employment levels in the area remained stable through the first quarter of 2008, the Federal Reserve Board in a June report cited retailers operating stores in the region said they expect the next several months to be challenging.

“Retail sales seem to be okay, but I don't see any substantial increases at this point,” says Donald Mace, vice president of leasing with KeyPoint Partners, LLC, a Burlington, Mass.-based commercial real estate services firm. “There is not a lot of upside right now,” he added.

So far, the effect has been minimal — from the fourth quarter of 2007 to the first quarter of 2008, the vacancy rate in Boston actually decreased 10 basis points, to 5 percent, according to Reis.

However, during that period, there was no increase in asking rents and the effective rents rose just 0.2 percent, to $19.99 per square foot, compared to an increase of 0.9 percent between the second and third quarters of 2007. Tenants now push harder to get good deals, according to Mace. Today, they won't accept rental increases greater than 12 percent, while last year increases of up to 15 percent were possible, he notes.

Going forward, Reis forecasts the vacancy rate in Boston will rise to 5.7 percent, in part due to an influx of new retail development. Approximately 2.1 million square feet of retail space is slated for delivery this year, according to Marcus & Millichap, up more than 10 percent from the 1.9 million square feet that came on line in 2007.

“Demand has definitely softened, but it is still relatively strong,” says Patrick J. Paladino, Jr., senior vice president of retail brokerage with Colliers, Meredith & Grew, a Boston-based commercial real estate firm. “Instead of ten people chasing a prime spot, there might be five. But, it hasn't gotten to the point where landlords are concerned.”

At existing properties, that has meant that landlords are focusing on renewals rather than new leases, according to Elizabeth Kelley, general manager of the Mall at Whitney Field in Leominster, Mass., a 657,547-square-foot regional mall managed by Chicago-based real estate firm Jones Lang LaSalle. New leasing activity at the Mall at Whitney Field has come mainly from service providers, such as dentists and acupuncturists, rather than traditional tenants, she notes.

The way the situation has been playing out with new development is that those retailers who committed to projects that broke ground last year or earlier are still going ahead with their plans, says Shannon. However, when approached about new locations, they are taking a much harder look. In fact, Shannon can't recall a new development coming on line since last August — most of the projects under construction right now have been in the works for a while.

The most recent center to break ground, the 675,000-square-foot lifestyle development Legacy Place at the intersection of Route 1 and I-95 in Dedham, Mass., was conceived back in 2005. Most of the property is pre-leased to tenants, including L.L. Bean, Borders and Whole Foods. Legacy Place is a joint venture between Chestnut Hill, Mass.-based W/S Development and Dedham-based theater operator National Amusements and is scheduled for completion in the summer of 2009.

“It's getting a lot more difficult for those projects that haven't started construction — I've heard of deals where the landlord would have the property under contract and a letter of intent from a tenant and the tenant would call back and say ‘We are putting our plans on hold,’” Shannon says.

The projects going strong involve single-tenant properties anchored by drugstores such as Walgreens and CVS Pharmacy, although they now insist on prime locations. Shannon says, “They are really going after the class-A, in-fill sites.”

Still waiting

The transforming market has impacted investment sales in the region, as experts insist Boston remains high on investors' lists of interest for retail properties.

The offers on properties are still coming in, Shannon notes — but in the past six months, he has not consummated any closings. During that period, only 16 retail properties traded hands in Boston, according to New York City-based real estate data provider Real Capital Analytics, with total dollar volume of $244 million.

Leased-up assets in prime locations continue to trade hands, according to Heald, but the strong demand for lesser-quality centers has gone down considerably and fewer investors are actively looking for acquisitions than in previous years. Heald estimates that cap rates on class-A assets have moved up 25 basis points to 50 basis points since 2007, while class-B and class-C properties may gave gone up as much as 125 basis points. Last year, cap rates for retail properties in the Boston area averaged between the mid- 6-percent to low 7-percent range, according to both Real Capital Analytics and Marcus & Millichap.

“There is no demand right now for a lot of the class-B and class-C type properties, because the sellers are still expecting unrealistic prices and the buyers are still not going for it,” Shannon says. “Boston is still a very desirable market, but there is a disconnect between what sellers are willing to sell for and what buyers are willing to pay. People are pessimistic about what they can achieve on rent, so the deals that are being done are more low-risk-type deals.”

Boston Demographics

Population: (2006 estimate) 590,763

Total housing units: 254,563

Median value of housing: $432,800

Median household income: $47,974

Per capita income: $29,243

In labor force (population 16 years and over): 318,490

Percentage of population with bachelor's or higher: 41.6%

Median age: 33.6 years

Mean travel time to work: 27.7 minutes

Source: U.S. Census Bureau, 2006 American Community Survey