Shopping center REITs turned in a respectable performance for the fourth quarter of 2009, giving credence to the notion that the worst of the downturn may be over. Yet REIT analysts continue to be cautious about the sector’s prospects for 2010, as the year may bring more closings among smaller shopping center tenants and make re-leasing vacant space difficult.

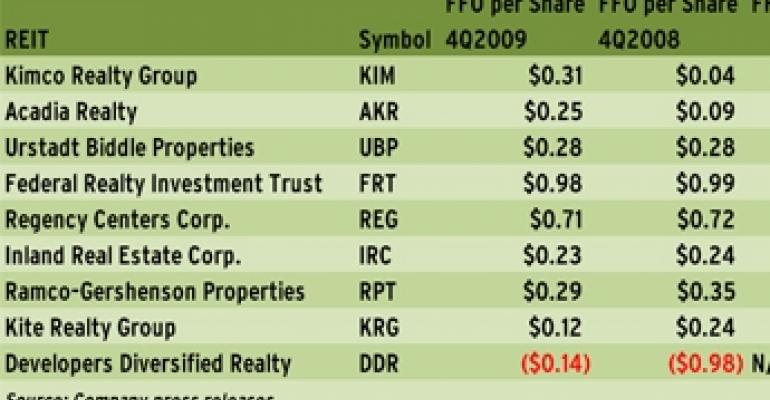

For the three months ended Dec. 31, 2009, two shopping center REITs beat consensus analyst estimates, two were on target and five missed. The outperformers included Kimco Realty Corp. (NYSE: KIM) and Federal Realty Investment Trust (NYSE: FRT), which beat estimates by $0.02 per share and $0.09 per share respectively. Developers Diversified Realty (NYSE: DDR), Regency Centers Corp., (NYSE: REG), Ramco-Gershenson Properties Trust (NYSE: RPT), Acadia Realty Trust (a href="http://www.google.com/finance?q=NYSE:AKR" target="_blank">NYSE: AKR) and Urstadt Biddle Properties Inc. (NYSE: UBA) were among those that missed. The misses, for the most part, amounted to no more than a penny.

Developers Diversified Realty missed by $0.47 per share, but according to Rich Moore, a REIT analyst with RBC Capital Markets, the consensus estimate of $0.33 per share represented an error and should be ignored. Developers Diversified’s fourth quarter FFO loss of $0.14 per share was in line with RBC estimates. Results for Kite Realty Group Trust (NYSE: KRG) and Inland Real Estate Corp. (NYSE: IRC) were in line with analyst expectations.

In general, the outlook appears to be brightening for shopping center REITs, as they report an increase in interest from expanding tenants, says Robert McMillan, a REIT analyst with New York City-based Standard & Poor’s Equity Research. “There is more positive sentiment regarding retailers looking for more space and that bodes well and should give them more pricing power,” McMillan notes. “I am looking for an improvement this year in terms of occupancy and rent trends.”

Overall, at year-end 2009, occupancy rates in the shopping center sector stayed above 90 percent, and some firms, including New Hyde Park, N.Y.-based Kimco Realty Corp., reported increasing success in re-leasing spaces left over from the bankruptcies of junior anchors Circuit City and Linen ‘n Things. Through most of last year, those empty big box spaces were among the biggest problems facing shopping center REITs, resulting in widespread NOI declines. Yet while the big box situation may be improving, 2010 might bring with it its own set of challenges when it comes to smaller, mom-and-pop tenants, says Jason Lail, senior real estate analyst with SNL Financial, a Charlottesville, Va.-based research firm. In addition, as retailers continue to keep a close eye on their store portfolios, re-leasing will likely still be a challenge.

“I think this year there is still a little bit of shaking out [left], to be honest,” Lail notes. “As a whole, shopping center REITs have held up relatively well, but I really think the shopping center space is saturated through the next couple of years. I am curious if there will be any major tenant bankruptcies this year and how the supply chain as whole will affect occupancy.”

Some REIT executives appear to share Lail’s concern. During Kimco Realty Corp.’s earnings call on Feb. 4, company CFO Michael Pappagallo gave an estimate for same-store NOI in 2010 that was between flat and down two percent as Kimco expects to see additional fall-out from potential store closings in the first half of the year. The good news, according to Paul Freddo, senior executive vice president of leasing and development with Beachwood, Ohio-based Developers Diversified Realty, is that retailers have learned to use inventory controls and cost reduction strategies to sail through a challenging economic climate.

There’s also been a significant slowdown in rent reduction requests from struggling tenants, according to Dawn M. Becker, executive vice president and chief operating officer with Federal Realty Investment Trust, a Rockville, Md.-based REIT. The requests that do come in are from tenants that were already facing problems last year and need more time to turn themselves around, not from new retailers. Now, the REITs are waiting to see tenants show sustained top line and earnings growth that will be a good predictor of future expansion.

To date, shopping center REITs that have yet to report their fourth quarter 2009 results include Cedar Shopping Centers(NYSE: CDR), Equity One Inc. (NYSE: EQYNYSE: BFS) and Weingarten Realty Investors (NYSE: WRI). Weingarten is scheduled to report after the market closes on Feb. 24. Cedar Shopping Centers and Equity One will release their results on March 3 and March 4 respectively. Saul Centers has not indicated a reporting date.

—Elaine Misonzhnik