Apparel seller New York & Co.’s January 11 announcement that it plans to open up to 25 outlet stores in fiscal 2010 is a sign of the times for the U.S. retail real estate industry.

New York & Co.—not a traditional outlet center player—had quietly tested an off-price concept at several Prime Outlet properties last year, including in Youngstown, Pa., Hagerstown, Md. and Orlando, Fla. Company executives expect all three locations look to achieve profitability in their first year of operation. And New York and Co. is not the only retailer expanding into the outlet space. On January 15, reports surfaced that luxury department store chain Bloomingdale’s might enter the upscale outlet center arena this year. And department store operator Lord & Taylor already announced it would open its first, 15,000-square-foot outlet store at the Jersey Gardens Outlet Mall in Elizabeth, N.J. in mid-February.

A new retail reality is driving the interest in outlet space. Unlike a year ago, publicly traded retail companies on solid footing are taking tentative steps to expand again. But high levels of unemployment likely to last for years combined with a diminished pool of household credit mean any rebound in consumer spending will be a drawn-out process. Consumers that will shop won’t spend lavishly.

But that’s not the only trend at play. Consumers still have an eye for brands. They may be trading down in price, but many consumers remain label conscious. That leaves outlet centers—with tenants that offer chic brands at low prices—poised to be the stars of the sector in the coming years. Outlet centers had already compiled a strong track record in recent years before the Great Recession hit. The emerging trends should only solidify their place, industry insiders say.

“We are just seeing a tremendous interest from brands, retailers and developers,” says Lisa Quier Wagner, president of Quier Target Marketing Inc., a Washington, D.C.-based consulting firm that specializes in outlet center marketing, and partner in EWB Development LLC, a Vermont-based developer of outlet centers. “I’ve been in the industry 21 years, and I’ve never seen an interest in outlets as acute as it is now.”

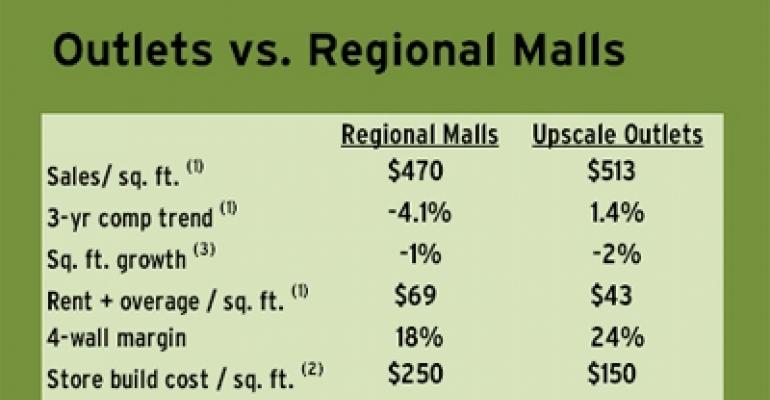

In fact, the first major retail real estate acquisition to be completed this year (and the largest acquisition since 2007) will be Simon Property Group’s $2.3 billion purchase of Prime Outlets Acquisition Co. from the Lightstone Group and Lightstone Value Plus REIT Inc. While other property types have struggled as consumers cut back on discretionary spending, upscale outlet centers continue to attract shoppers with their promise of deep discounts on popular brands. In the third quarter of 2009, Simon Property Group reported that sales per square foot at its outlet properties averaged $492. Sales at its regional malls averaged $438 per square foot.

In addition, comparable sales growth at outlet centers has been outpacing gains at regional malls by an average of 400 basis points annually since 2006, according to a Jan. 11 report from Credit Suisse, entitled The Hidden Gem of Retail. At Simon, for example, outlet center sales grew 7.0 percent in 2007 vs. 3.2 percent for regional mall sales. In 2008 outlet center sales rose 1.8 percent vs. a 4.3 percent decline for regional malls. And in 2009 while comparable sales at outlet centers were down 4.5 percent, that figure was much better than the 11.2 percent decline at Simon’s regional malls. Meanwhile, the occupancy rate at its outlet portfolio was 97.5 percent compared with 91.4 percent for its regional malls.

Moreover, outlet centers provide an attractive bargain for prospective tenants since they offer more flexible leasing terms than regional malls. Rents at outlet centers are usually lower than at regional malls. At Simon, regional mall rents (for inline tenants) averaged $40.05 per square foot vs. $32.95 per square foot at its outlet centers as of Sept. 30, 2009. In addition, outlet center rents are more tied to the stores’ sales performance, notes Quier Wagner. Plus, common area charges and build-out costs for outlet tenants are a fraction of what they are at regional malls.

Going forward, “we anticipate continued growth from companies that wish to roll out more outlet stores, as well as new brands taking a fresh look at the outlet industry,” says Michele Rothstein, senior vice president of marketing with Chelsea Property Group, Simon’s outlet division. Among recent newcomers to Chelsea’s portfolio, Rothstein counts women’s apparel chain Talbots and shoe seller Rocket Dog.

Retailers’ view of outlet centers has also shifted in recent years, Credit Suisse analysts note. In the past, retailers used outlet stores primarily for getting rid of excess inventory. Today, they have “become more of a pure-play specialty channel that has many of the best brands, but with low development, rent and maintenance costs.”

Another selling point—there is much more room for potential expansion in the outlet center sector. While there are approximately 1,400 regional malls in the U.S., there are only about 150 upscale outlet centers, according to Credit Suisse’s estimates.

The Credit Suisse analysts see this channel as offering great growth potential for certain retailers, including apparel seller J. Crew, its children’s spin-off concept Crewcuts and athletic apparel chain lululemon. The most successful outlet tenants combine limited exposure at regional malls with strong brand awareness among consumers, the report notes.

“It’s all about the brand” says Quier Wagner. “The consumer is attracted to the brand and the discount, but the brand first. The multi-brand and discount stores don’t fare as well because the consumers look at the store and they don’t understand what it’s selling.”

That might become a potential obstacle for New York & Company, according to Howard Davidowitz, chairman of Davidowitz & Associates Inc., a New York City-based retail consulting and investment banking firm. While some mid-price private label brands, including the Gap and Ann Taylor, have succeeded in the outlet format, those brands tend to be household names. Whether the New York & Co. brand will have the same pull with consumers remains to be seen, Davidowitz notes.

“An outlet center is different from the mall. A lot of the people who go to outlets go there on buses because the attraction is to get these [big-name] brands at 30, 40 percent off,” he says. “But New York & Co. is a budget apparel chain. So maybe it will work, maybe sales will be a little better than what they do normally, but I give this a 50/50 shot.”

Another predictor of success is whether the retailer sells unique merchandise through its outlet stores, or the same products found at its mall stores, says Jeff Green, president of Jeff Green Partners, a Mill Valley, Calif.-based consulting firm. He brings up Gap Inc. as an example of outlets done right—“it’s almost like another brand, not just a Gap store.” New York & Company plans to eventually produce merchandise specific to its outlet format.

—Elaine Misonzhnik