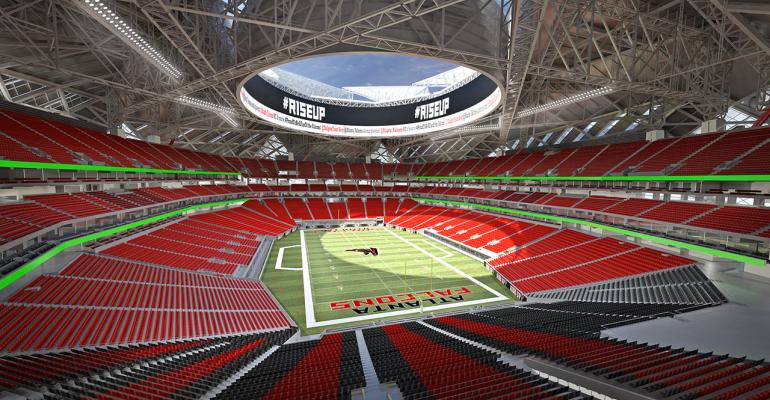

(Bloomberg)—The Atlanta Falcons have closed financing on their new $1.5 billion stadium a year earlier than executives originally projected.

Funding for the stadium, which opens next year, includes $200 million in public money backed by hotel and motel taxes and $200 million from the National Football League, according to the team. The other $1.1 billion will come from newly financed debt, seat license sales and equity contributed by Falcons owner Arthur Blank and his partners.

AMB Sports & Entertainment, the parent company of Blank’s business, has restructured an $850 million construction loan that it took out last year, according to Executive Vice President Greg Beadles. A third of that total will remain with bank partners Bank of America Corp. and SunTrust Banks Inc., which oversaw the original loan, while the other $566 million was converted to 26-year corporate bonds that were privately placed.

“We had phenomenal demand,” said Beadles, who led the financing effort. “We went out looking for a little more than half a billion in long-term debt, and we received bids back that were about $2.5 billion in total.”

AMBSE took on 18 institutional investors, mostly insurance companies and pension funds, which have invested in other stadium project across the major U.S. leagues.

To contact the reporter on this story: Eben Novy-Williams in New York at [email protected] To contact the editors responsible for this story: Nick Turner at [email protected]

COPYRIGHT

© 2016 Bloomberg L.P