It seems to be only a matter of time before higher inflation makes its way into official U.S. figures. Countries like Brazil and China are already struggling with it, and even countries with unused capacity like the United Kingdom have to deal with faster than expected price increases.

Food prices are spiking, and the price of oil had been inching upward even before unrest in the Middle East sparked fears of shortages.

Moody’s Economy.com predicts that the headline Consumer Price Index, which counts food and energy prices, will rise at a relatively modest rate of approximately 2% per year in 2011 and 2012, up from 1.6% in 2010.

But when Wal-Mart CEO Bill Simon warns that “inflation is going to be serious,” citing “cost increases that are coming through at a rapid rate,”1 it seems prudent to add a percentage point or so to inflation forecasts and pick investments accordingly.

Standard textbooks say that commercial real estate offers a good hedge against inflation. Will this hold true given the current environment?

The basis of received wisdom

When the returns from investing in an asset exceed the rate of inflation, it is considered to be a good hedge. In the 1980s, a slew of papers2 examined the rate of return on various property types and concluded that commercial real estate investors were in fact compensated for inflation risk.

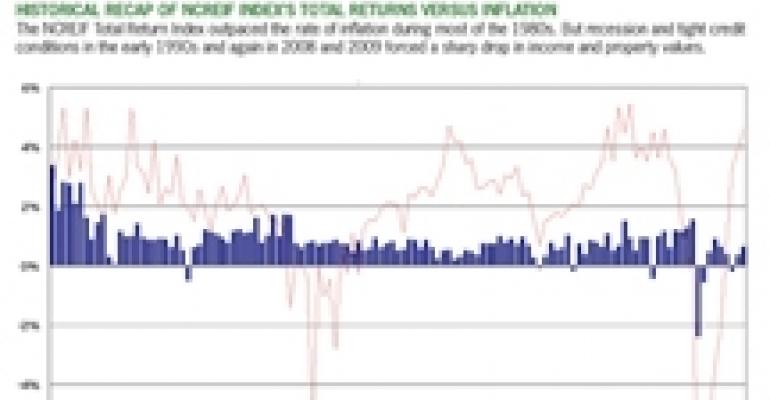

Indeed, The National Council of Real Estate Investment Fiduciaries’ total return index, which attempts to capture the gain from both net operating income as well as increases in asset value, generally posted higher returns than inflation in most of the 1980s. The index tracks a large pool of institutional quality commercial real estate held mostly by pension funds.

But what happened in the early 1990s? Shortage in credit from the savings and loan crisis resulted in a sharp dip in commercial real estate income and values. It wasn’t until the mid-1990s that the asset class began posting returns above inflation.

Expect 2011 to be a robust year

The key issue therefore is what determines returns from commercial real estate. With the unemployment rate expected to remain high for another few years, Reis projects only a measured increase in the demand for space.

Income returns have begun to rise from the troughs of 2009 as occupancies and rent growth stabilized, but property types are recovering at different rates.

The continuing woes of the housing market imply a few robust years of growth for the multifamily sector. Office vacancies have begun to decline, but retail vacancies are expected to break the historic high of 11.1% last observed in 1990.

What about capital returns? Although capitalization rates have begun to inch downward, trends remain divided in many markets.

Trophy properties in gateway cities trade at cap rates under 5%, while distressed deals transact at cap rates of 8% or above. (The cap rate is the initial return to the investor based on the purchase price and the annual net operating income the property generates.)

Few investors are counting on high capital returns from trophy properties. The premium they paid via a lower cap rate rests on the perception of more stable income returns from a fully occupied building with reliable tenant rolls.

But paying a higher price for trophy properties translates to a lower rate of income return. Distressed deals might offer value-added investors potentially higher rates of both income and capital returns, but these are opportunistic ventures. These aren’t the type of deals we usually discuss when we refer to using real estate to hedge against inflation.

“The consensus is that total annual returns from commercial real estate over the next two years will be fairly robust, in the 10 to 11 percent range,” says Reis senior economist Ryan Severino, who serves on the National Council of Real Estate Investment Fiduciaries’ research committee.

“More than half of that [return] will come from income returns as vacancies tighten and rent growth accelerates, but don’t expect big jumps in commercial real estate values,” adds Severino.

Understand the risks and rewards

An asset that returns 10% to 11% certainly implies a good hedge against rising prices, even if consensus inflation expectations from professional business forecasters double from its current 2%.3

However, with many commercial real estate property types still in flux, it is easy to make a mistake. Bet on a property in a market that continues to post rising vacancy, and expect your hedging strategy to fail. Overpay for a trophy property and expect your spread against inflation to narrow.

Multifamily as a whole might be all the rage right now, but finding a high-quality retail property fully occupied by reliable tenants locked in for several years may be a better option, depending on prevailing prices.

Concerns about rising inflation emphasize the importance of — but do not really change — the basic mandate of good real estate investing. Know your property types and market trends, and find assets that offer a good rate of income and capital return.

Footnotes:

1 “Wal-Mart CEO Bill Simon Expects Inflation,” by Jayne O’Connell, USA Today, March 31, 2011.

2 See Bruegemann, et al, “Real Estate Investment Funds: Performance and Portfolio Considerations,” AREUEA Journal (Spring 1984), Hartzell, et al, “Real Estate Returns and Inflation,” AREUEA Journal (Spring 1987) and Rubens et al, “The Inflation-Hedging Effectiveness of Real Estate, Journal of Real Estate Research 4:2 (1989).

3 See the Federal Reserve Bank of Philadelphia’s First Quarter 2011 Survey of Professional Forecasters, released last February 11, 2011.

Victor Calanog is head of research and economics for New York-based research firm Reis.