At last, good news for affordable housing! The market is strong and getting even stronger for properties with low rents, including apartments built with government funds for low-income families.

“We’re seeing vacancy rates at record lows,” says Bryan Keller, CPA, partner-in-charge of RubinBrown’s Real Estate Services Group, which has just released its 2012 Apartment Statistical Data report.

RubinBrown surveys a unique slice of the housing market—so don’t throw its data onto the pile with reports from other number crunchers like Reis Inc., and Axiometrics Inc. Of the 407 properties surveyed by RubinBrown, 372 were “government-assisted” housing, including 363 built with federal low-income housing tax credits. The other, unsubsidized apartment properties in the report are also relatively inexpensive, with average rents of $674 a month, which is even lower than the $721 a month average for the subsidized apartments.

Generation Y factors in

These properties benefit from the same trends keeping vacancy rates low in the rest of the apartment market. RubinBrown cites the flood of Generation Y renters and a lack of competition from for-sale housing. Homeownership rates matter even for low-income tax credit housing, which is reserved for households earning a maximum of 60 percent of the local median income. In tertiary markets, that may be enough to afford a starter home. Also, when competition from for-sale housing is strong, it has a ripple effect on the whole housing market.

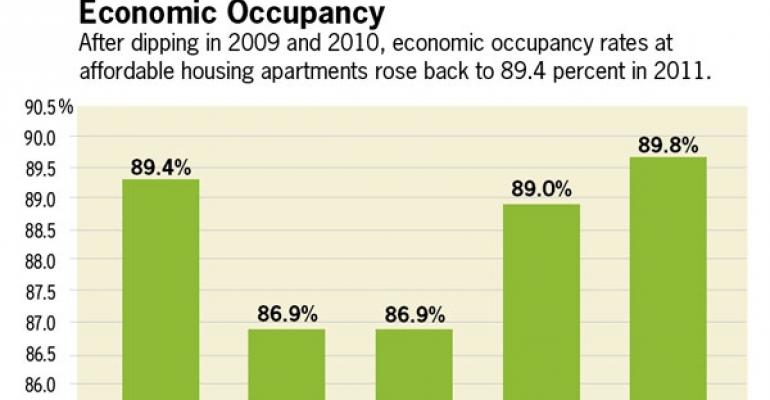

Economic occupancies are rising for these properties. In 2011, economic occupancies rose to 89.4 percent on average across the country, up nearly three percentage points from 2010 and 2009, according to the report.

“We’re expecting to break 90 percent in 2012 for the first time in several years,” says Keller.

Occupancy rates can vary a lot from one local market to another. “You’ve got properties in there that are in rural Ohio and properties in downtown Los Angeles,” says Keller. The Western states, including California and Washington, had an average occupancy rate of 96.6 percent in 2001. Occupancies in the Southeast are much lower on average at 86.3 percent. A tough economy and low rates of household formation have hurt many tertiary markets.

The market for affordable properties could also face challenges in the future. “They shouldn’t get ahead of themselves,” says Keller. As homeownership once again becomes desirable and more easily achievable, the growth experienced by the multifamily housing industry will eventually begin to slow.

Congress could also damage affordable housing programs. “With tax reform imminent, probabilities are high that all multifamily stakeholders will feel the impact to some degree, whether through reduced credits, subsidies or deductions,” says Keller.

Affordable housing's sizable market

Maybe you think of government-subsidized affordable housing as an odd little business that doesn’t amount to much. Think again. The first four names on the National Multi-Housing Council’s list of the Top 50 owners of apartment properties are all big investors in government-subsidized affordable housing: Boston Capital Corp., Centerline Capital Group, Boston Financial Investment Management and SunAmerica Affordable Housing Partners. Equity Residential, the largest multifamily real estate investment trust in the country, came in fifth.

Before the housing crisis, a third of all multifamily housing units completed in any given year were built with help from a mix of federal, state and local housing funds. Developers built more than 100,000 new units a year with help from the federal low-income housing tax credit program, according to the National Council of State Housing Agencies. Yet developers continued through the economic crisis.

As David Cardwell, vice president of capital markets for the National Multi-Housing Council puts it, “It didn’t crash in the crash.”