Changing demographics and shifting land use patterns will significantly influence development of retail investment strategies going forward.

These trends taken together represent a progression toward greater urbanization in the U.S., a movement back toward the cities and to higher density living and diverse patterns of mixed-use development.

This evolving trend stems from contemporary choices of Baby Boomers and Echo Boomers, rising transportation costs, and community and government preferences toward mixed-use, higher-density, walkable communities and away from suburban sprawl.

The renewed urbanization represents a significant turn from suburbanization patterns of the past decades. Retailers are already adapting their formats to respond to these changes.

Investors will also need to reformulate retail strategies, given changing patterns of demand and land use. A closer look follows.

Urban Amenities: Intergenerational Attraction

The social preference will be the strongest attraction for Baby Boomers to urban areas. Retiring Baby Boomers will have a net migration to rural areas if they follow behavior of their predecessors, according to John Cromartie and Peter Nelson in their 2009 study, “Baby Boom Migration and Its Impact on Rural America,” published by the Department of Agriculture’s Economic Research Service.

However, that same study and Ania Wieckowski’s “Back to the City” in the May 2010 Harvard Business Review concluded that aging Boomers will appreciate urban amenities such as proximity to health care and families, and walkable, active communities.

Many Baby Boomers exhibit empty nest syndrome when their Generation Y children leave home. In real estate, this typically is thought to entail leaving behind their large suburban home for smaller, more manageable living quarters in vibrant, entertainment-driven environments.

As retirement looms for the older Boomers, 17 million, or 25 % of the cohort, will be senior citizens within the next decade.

Baby Boomers have indicated in analyses that they are most concerned with obtaining affordable housing. They will also want to be in communities that are walkable or have public transit for both philosophical and physical reasons.

It is likely they will prefer and eventually have to stop driving. For this reason, it is likely they will seek smaller, easier shopping formats that are closer to home.

Indeed, walkability has become an important factor. Zillow, the popular online real estate database, in July 2007 began rating the walkability of the property to retail and transit infrastructure and other services on a scale of 0 to 100.

For these reasons, we believe the Baby Boomers will either be inclined to move to or remain in urban areas. Also in the near term, they are unlikely to retire at typical retirement age.

When they do retire, we expect at most they will exhibit a relatively insignificant urban outmigration from cities compared with the influx of Echo Boomers.

Dave Schreiner, vice president of active adult business development for Pulte Homes, bets his company will profit from baby boomers’ preference for more urban environments.

“A large number of Del Webb (the Pulte active adult brand) residents are starting new businesses, getting retrained and staying connected to the workforce. They don’t leave it entirely,” says Schreiner.

“That’s one advantage of positioning our newer communities close to large metropolitan centers. That’s where the jobs are.”

Different generation, different motives

The factors driving Echo Boomers toward urban areas is somewhat different. The desire for vibrant and cultural social experiences is the same, but their economic motivation for urban living is much stronger and clearer.

The overwhelming majority of Echo Boomers are primarily focused on career development and economic opportunity. This is illustrated by shifts in U.S. Census Bureau statistics that report 64% of 25-to 34-year-olds look for the city they desire to live in before looking for an actual job.

From 1990 to 2000, the Echo Boomers showed a 250% increase in positive likelihood to live within three miles of a central business district. This indicates that there is an assumption that a city holds opportunities Echo Boomers desire.

In line with these noted urbanization trends of U.S. population is the forecasting by the population division of the Department of Economics and Social Affairs of the United Nations.

The department lists the United States in the top five countries in the world for rapid speed of population decline in rural areas at -0.67% over the last 10 years. The urban population, meanwhile, has increased at an average of 1.38% over the same period.

Impact of rising fuel costs

Increasing transportation costs also are a major force behind urbanization trends. Despite increased resources devoted to developing alternative energy, it is clear that the majority of the energy to meet demand for the foreseeable future will come from fossil fuels.

There appears to be no major commercial innovations on the horizon that will interrupt the upward pressure on oil prices.

An assumption can be made that due to increased automotive travel costs, people will drive less and prefer to live in areas where they are closer to work, necessities and entertainment.

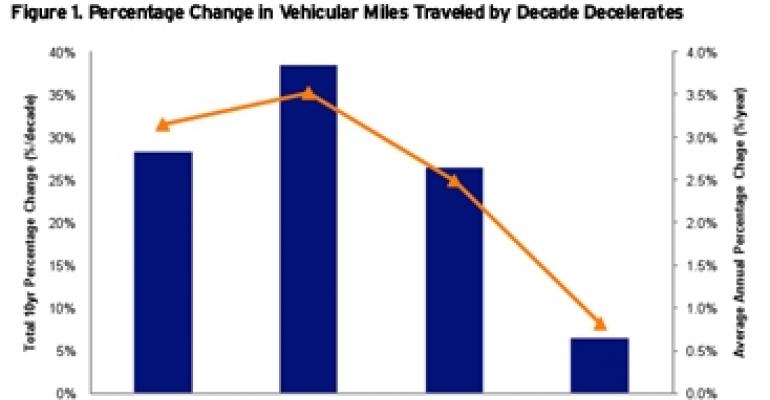

The fact is that this has already been happening, according to data from the Federal Highway Administration. Total vehicular miles traveled (VMT) in the United States has generally increased year-over-year for the past 30 years. However, this increase has begun to decelerate rapidly over the last two decades.

As seen in Figure 1, the last increase in VMT occurred between the 1970s and the 1980s. Since then, the percentage increase of annual VMT has decelerated.

The peak decade-over-decade increase was 38.5% from 1981 to 1990. The following decade the VMT increased by 26.5%, and from 2001 to 2010, the VMT has only increased a total of 6.5%.

This deceleration is occurring despite a growth in population and income, and despite overall economic expansion of the United States. A direct conclusion is that people are shifting their means of travel away from the automobile.

At the same time, public transportation systems have become better developed, and transit-oriented development is also being pursued in numerous metro areas.

Changes are by design

Some of the shift toward mixed-use and high-density design can be attributed to widespread changes in industry standards of city planners, urban designers and the real estate sector.

Over the last 10 to 15 years, the generally accepted idea of what constitutes a good neighborhood has changed quite a bit, and it is not suburban sprawl.

It has become clear to industry professionals that mixed-use design, walkable communities and access to public transport is not a fad and will continue to be important in the future.

Most architecture and planning colleges and universities train new planners in the design of integrated mixed-use communities. Architecture and planning schools have ubiquitously taught some form of “New Urbanism.” The next generation of planners is likewise being inundated with the tenants of thoughtful urban design.

Real estate trade organizations, especially the Urban Land Institute, have produced numerous publications on the value of developments that effectively combine density, open space, multiple transportation options and walkability among a mix of real estate uses.

While zoning was for many decades strictly confined to regulating separation between different land uses, many community planning boards, especially those in need of urban revival, are increasingly enticing developers with zoning law variances, tax incentives and public-private partnerships to undertake retail and mixed-used development.

Consequences for the retail sector

As a proxy for demand for retail in urban areas, we have examined retail rent growth in first tier and top-performing metropolitan statistical areas (MSAs) across the U.S.

We examined the trailing five-year recorded rent growth from CBRE Econometric Advisors and the ING Clarion Research and Strategy Group’s projected five-year rent growth for a given MSA overall. Then we compared that to submarkets of the MSA that could be considered the central business district (CBD).

Because of data deficiencies and complications, New York City and Los Angeles were omitted from this study. The results can be seen in Figure 2.

The results indicate that 53% of the time in the last five years, the rent growth for retail assets in the CBD has outpaced the overall MSA rent growth. The magnitude of average rent growth has been about 2.5 times greater in the CBD than in the MSA.

For the five-year forecast, the CBD rent growth outpaces the MSA 67% of the time, and is on average 1.5 times greater in magnitude.

This projection suggests that more often than not the demand for — and lack of supply of — retail space in CBDs will exhibit significantly more robust rent growth than less dense areas of the greater MSA encompassing that CBD.

This is a reasonable conclusion considering the proven and projected increased in demand for urban places and the relatively limited supply of such locations.

The results of this data analysis indicate a potential business preference for denser urban locations over outer edges of the MSA. Given our analysis of demographic and land use trends, we expect this divergence to continue and potentially widen in the future.

David Lynn is a managing director, generalist portfolio manager and head of investment strategy for ING Clarion Partners in New York.