The “unusual suspects” impacting commercial real estate.

Most investors would agree that commercial real estate is a long-term play. Yet there are some significant structural changes afoot that have the potential to reshape the real estate landscape – and influence future capital flows – as it relates to both the near- and long-term horizon.

Evidence of structural change is readily apparent from the rise in cross-border investment that is putting pressure on cap rates to mobile technology that is changing basic supply and demand fundamentals for real estate. “The pace of change has continued to accelerate and shows no signs of abating. That dictates flexibility, study and anticipating change in a much more information-dense environment,” says CBRE Capital Markets Global President Chris Ludeman.

In their new white paper Navigating Structural Change, CBRE takes an in-depth look at three key structural changes impacting commercial real estate investors. Those three changes include the growing importance of new sources of foreign capital; regulatory and tax changes; and dynamic shifts in tenant demand that is occurring in retail, office and multifamily. Although this report focuses primarily on the impacts these long-term changes are having on the U.S. market, many of the issues and implications also apply to real estate markets across Europe and Asia.

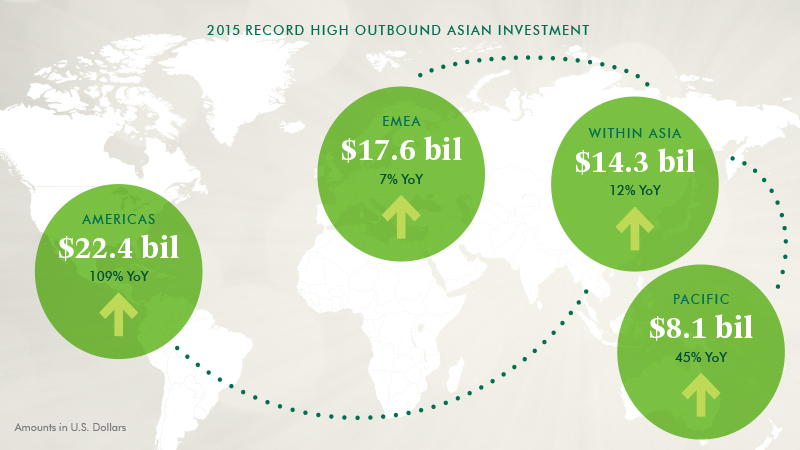

New Sources of Capital: Years of rapid economic growth and high rates of savings has shifted the world’s “center of gravity” of global capital more firmly to the Middle East and Asia. That wave of capital is coming from a variety of groups, including high-net-worth individuals, sovereign wealth funds, institutions and corporations, that all have very different costs of capital, time horizons, skill sets and investment vehicles.

Those entities share a common ambition to diversify and expand their holdings in markets outside their home countries. As such, foreign investors have become a structural driver that is substantially increasing demand in the U.S. An estimated $9.0 billion in Chinese investments and $9.6 billion in Middle Eastern investment were made in the U.S. commercial real estate market in 2015, according to CBRE Research, and the firm anticipates a similar volume in 2016.

Regulatory and tax changes are contributing to global capital flows by allowing more capital to leave home countries and making it easier to invest in different global destinations. In the U.S., a recent change that is likely to shift the global capital flow landscape is the extension of tax waivers under the FIRPTA revisions of December 2015. The law will give qualified foreign pension plans more favorable tax treatments for direct and REIT investments.

In addition, Basel III, Dodd-Frank and other banking regulations are structural issues to watch going forward. These regulations will attract additional scrutiny of banks and are likely to shift the rules of the game for global commercial real estate. The new Basel III rules will increase the risk weighting of real estate holdings, thereby increasing the cost of lending to commercial real estate. The Dodd-Frank risk-retention rules, which require securitized lenders to hold a piece of CMBS loans on their balance sheets, also could impact the volume of debt available in the U.S.

Tenant demand for different types of commercial real estate is constantly changing. However, there are some substantive shifts that have long-term implications for investment strategies. E-commerce continues to encroach on traditional brick-and-mortar retail as it now accounts for approximately 8 percent of all retail sales. Retail developers have almost completely shut off the pipeline of new construction in recent years, which has substantially tightened the institutional grade retail stock. At the same time, retailers continue to adapt to competition from online retailers with store closings and smaller store footprints.

In the office market, companies are downsizing and reconfiguring space to adapt to today’s more mobile workforce. The growing reliance on cloud computing and mobile technologies is reducing workers’ need for a fixed office and IT infrastructure. Companies are continuing to adapt to this new environment where individuals are working wherever, whenever and however they choose.

Multifamily may be going through the largest structural shift of all asset types following the housing bubble and resulting great recession. The percentage of homebuyers vs. renters has shifted materially in the U.S. to favor renters, not only among Millennials, but also among older renters who are now “renters by choice.” This changing dynamic may prolong the current construction cycle as developers create more supply to keep up with the growing demand.

All of these structural changes have the potential to impact the current real estate cycle in different ways. For investors, operating in this dynamic environment means thinking much more deeply and multi-dimensionally about investment opportunities. In addition, investors may need to be willing to be a bit contrarian in order to create alpha returns, says Ludeman. It also is important to note another dynamic change – real estate has become more liquid than it in past generations. “There are more vehicles to invest in real estate, which align with people’s long, intermediate and short-term goals and more innovation is likely to follow,” he adds.

CBRE has launched a three-part thought paper series on “Leading Global Capital in a Time of Uncertainty”. The thought leadership series provides insight on the shifting market dynamic to help investors make thoughtful decisions for both near- and long-term real estate investing strategies. The second report in the series, “Navigating Structural Change”, looks at three key structural changes: the growing importance in capital from the Middle East and Asia: regulatory and tax changes; and dynamic shifts in tenant demand that is occurring in retail, office and multifamily. Click here to access a full copy of the report.