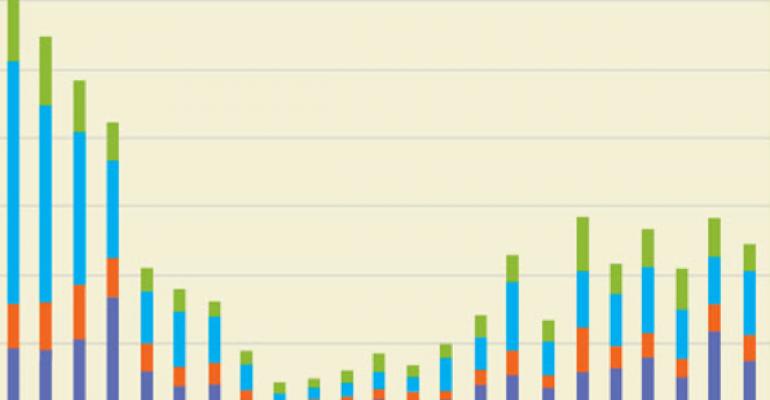

Although far from the 2007 peak, preliminary sales transaction volumes for the third quarter came in well above the 2009 trough levels with recent data showing strength in apartments after a July lull; increases in suburban office related to medical office portfolio activity (CBD preference is still strong); growth in industrial outside of flex; and weaker retail overall, but modest gains in malls outside of strip malls. Expect overall U.S. sales transaction volume growth to decline from 60 percent + in 2011 to around 10 percent for full-year 2012; while growth is slow, it remains positive in a more challenged macro-economic environment. Tech and energy are a few of the growth drivers for 2013 and beyond as outlined in Jones Lang LaSalle’s recently published Cross Sector Outlook.