Today’s lodging industry is wrestling with weakened revenues and the growing necessity of cost control. Now more than ever, hotel owners and operators are scrutinizing every possible means to reduce expenses.

Unlike previous recessions of the past quarter century, the current downturn and the virtual absence of credit for hotels have caused hotel property values to suffer disproportionately by inhibiting the buying, selling, and refinancing of hotels. Current tax assessments usually do not reflect this erosion of value.

Unfortunately, property taxes continue to be one of the least understood hotel expenses, and many hotel owners forego what could be significant savings by failing to explore the potential for lowering the real property tax assessment. A hotel’s property tax bill is one expenditure that potentially offers substantial savings.

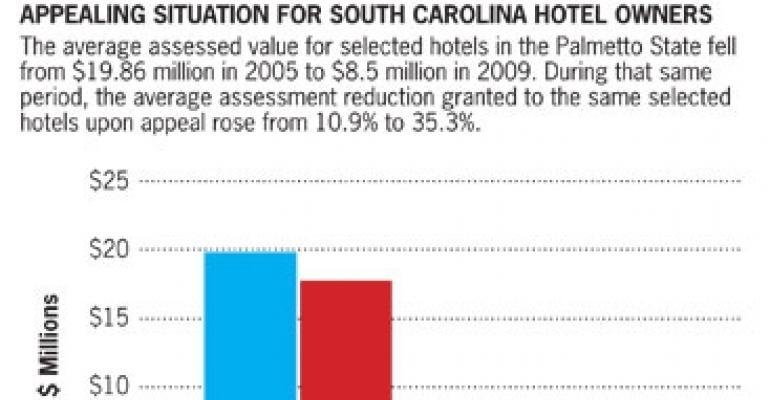

Among selected hotels in South Carolina, a comparison of the average assessed value and the average value after appeal in 2005 and 2009 demonstrates the precipitous decline in the real estate market (see chart).

Property tax statutes vary from state to state and are generally complicated. Any analysis of potential savings requires detailed knowledge of state statutes and regulations. In most markets, however, two essential concepts will lead the way to a successful appeal: (1) a realistic look at comparable sales; and (2) excluding non-real estate factors from the hotel’s real property tax bill.

Question sales comps

First, consider that nearly every state approaches assessments as if the property had been sold on the open market as of an assumed valuation date. In South Carolina, December 31 of the prior calendar year is the assumed valuation date. This statutory assumption, made at a time where few if any sales are taking place, presents a myriad of problems in light of current credit constraints and the pressures of a depressed real estate market.

The Appraisal Institute’s Standards of Professional Appraisal Practice define fair market value as the most probable sale price that a property would bring in a competitive and open market. The standards assume that such a transaction would involve a willing buyer and a willing seller, free of compulsion.

Most U.S. markets today lack the liquidity and investor demand for hotel properties that would constitute a competitive and open market. Put differently, a leveraged purchase at attractive terms for the borrower does not represent a reasonable hypothetical model for the assessor charged with valuing a hotel property today.

Moreover, few sales in the current market involve a willing buyer and a willing seller engaging in a transaction without duress, and consequently such sales fail to satisfy the Appraisal Institute’s definition of fair market value.

Extract the extras

Assessors are charged with valuing the hotel’s real estate, but hotels are typically sold as going concerns rather than as real estate. In other words, investors buy hotels based on actual or potential revenue as businesses. Put differently, investors do not buy the hotel’s real estate separate from its business value.

It is worth noting that an appraisal for a hotel’s value for a pending sale or prospective financing will value the hotel’s going concern rather than the hotel’s real property, making the appraisal’s valuation inappropriate for use in a tax appeal.

Few hotel owners are familiar with the critical and often controversial concept of subtracting the value of a hotel’s operating business and its personal property in order to isolate the asset’s real estate value. Yet that is precisely the method assessors should be using.

Most assessors agree that the business enterprise value must be excluded to determine a hotel’s taxable value, but the appropriate methodology for that calculation is a source of considerable controversy within the appraisal industry.

Most appraisers favor the income approach in valuing hotels. Unlike many income-producing properties, such as offices or apartment complexes, a hotel depends on the combination of the real property, the personal property and the business acumen of management to generate revenues.

Of those three factors, only the revenue attributable to the property itself is relevant to taxable property value. For example, a hotel’s income may be heavily dependent on the use of a website or a reservation system, but such factors must be ignored in valuing the hotel for property tax purposes.

There is no consensus regarding the appropriate method of calculating business enterprise value. A hotel owner who adopts too aggressive an approach runs the risk of the assessor turning a deaf ear to an otherwise merit-worthy appeal.

Cap rate considerations

The uncertainty surrounding the hotel capitalization rate — the buyer’s initial annual rate of return based on the purchase price — further complicates the income approach to valuing hotels in the current distressed market. Of the seven methods endorsed by the Appraisal Institute for calculating a capitalization rate, six require comparable sales. Such sales often do not exist in the current real estate market.

The use of a capitalization-rate approach to determine value in a market where there are few, if any, sales with willing sellers and willing buyers begs the question of whether any capitalization rate selected truly reflects fair market value.

The lack of available financing or credit in today’s market makes accurate calculation of a property’s value using the Appraisal Institute’s capitalization-rate-based methods extremely difficult, but the trend is inescapable: lower values.

Whether a tax appeal makes sense for a particular property requires careful and professional analysis. Yet with few comparable sales, little in the way of credit available for hotel properties and substantial pressure on capitalization rates, it is in a hotel owner’s best interest to work with an expert and carefully examine the values assigned by assessors to hotel properties. These steps may help hotel owners avoid paying an unfairly high tax bill.

Morris Ellison is a principal in the Charleston, S.C. law firm of Buist Moore Smythe McGee PA, the South Carolina member of American Property Tax Counsel (APTC). He can be reached at [email protected]. William T. Dawson III is an associate with the firm and can be reached at [email protected].