The tumultuous events of the last four weeks have prompted downward revisions to economic forecasts, and for good reason. On July 29, U.S. GDP growth figures for the second quarter came in at an anemic 1.3%, with first-quarter figures revised down to 0.4%.

Then came the debacle over the debt ceiling debate, and the S&P downgrade. The probability of a double-dip recession has now risen to between 30% and 50% based on consensus estimates, up from a relatively low 15% earlier in the year.

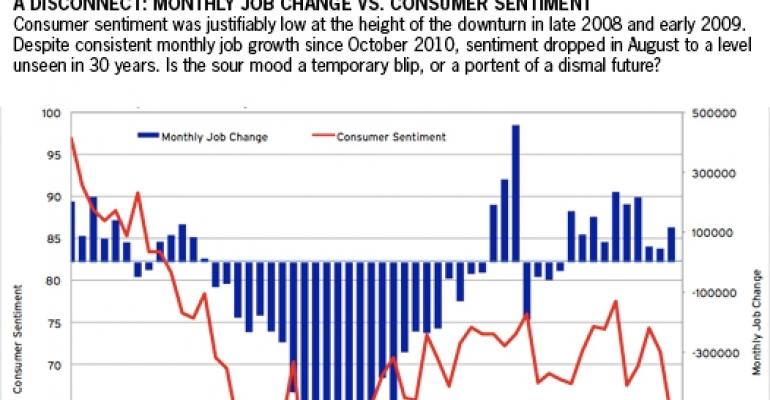

And yet there is good reason to believe that the economic recovery will continue to putter at an uninspiring pace, but progress nonetheless. Monthly job growth has been positive for 10 straight months since October 2010. Some 930,000 jobs have been created in the first seven months of 2011, about as much as the 940,000 jobs that were created in all of 2010.

Yes, it is disappointing that projections made early this year calling for 3.5% to 4% annualized GDP growth never materialized, but this is hardly like late 2008. Back then, major institutions were failing and had to be bailed out, and the economy shed hundreds of thousands of jobs beginning in January 2008.

Sentiment is a powerful force

The main problem is not an economy on the ropes, but a weak recovery plagued by institutional gridlock, and changing expectations of whether U.S. policymakers can encourage job creation while managing debt and deficit levels. We are at a critical juncture given the decidedly mixed nature of economic and financial data.

If we lose confidence as individuals and curtail spending quickly, and if businesses lower expectations and pull back on hiring, then we just earned ourselves the kind of low growth and high inflation environment that characterizes periods of stagflation.

Already we’ve observed a 0.2% drop in consumer spending in June. Preliminary August numbers from the University of Michigan’s consumer sentiment survey indicate a sharp drop to 54.9, its lowest level in 30 years.

A second recession is certainly not outside the realm of possibility, particularly if consumer and business spending pulls back. If this happens, however, then this would be a recession largely of our own doing, and we will really only have our fears, proclivities and frustratingly gridlocked systems to blame.

Commercial real estate effects

Obviously, a double-dip recession would suspend any hopes of a quick and robust recovery in fundamentals. But today’s uncertainty actually raises questions about how investment sales will fare. The sharp drop in equity markets may actually prompt greater demand for assets considered “safe havens,” generating a positive halo effect for Class-A properties in gateway cities and nudging cap rates downward.

For now, reports from brokers indicate that few buyers are pulling back or lowering pending bids on attractive properties because of the events of the last few weeks.

As new information arrives over the next two months, we will find out whether the optimists are prevailing or if the pessimists will win the day. Consensus estimates now place 2011 U.S. GDP growth at 1.6% to 1.8%, but that still implies that second-half GDP growth will accelerate to around 2.5%. For now, a double-dip recession is unlikely to happen, but sentiment is a fickle thing.

Victor Calanog is head of research and economics for New York-based research firm Reis.