Unfortunately, what should have been significant and encouraging news on the commercial real estate recovery front last month was hardly noticed on the newswires. First, a top New York bond trader, Cantor Fitzgerald, jumped into commercial mortgage originations.

The firm, largely unscathed by the capital markets meltdown, is joining forces with CIM Group, a Los Angeles real estate fund manager. The joint venture will originate about $5 billion in loans over the next year to be sold to investors as structured bonds.

Second, the largest commercial mortgage default on record quietly moved into foreclosure with little fanfare. Pershing Square Hedge Fund and Winthrop Realty Trust bought $300 million of mezzanine loans in the New York residential complex, Stuyvesant Town and Peter Cooper Village, for $45 million, or 15 cents on the dollar. The buyers immediately filed foreclosure against the property's owners, Tishman Speyer and BlackRock Realty, and are seeking control of the sprawling trophy complex.

Third, Colony Capital and Dune Real Estate Partners recently came out with scathing remarks about the lenders that provided construction loans for its unfinished Meadowlands Xanadu project in New Jersey. The borrowers say the lenders “refused” to renegotiate the construction loans, and the borrowers were “forced” to hand the $2 billion retail and entertainment project back.

What's newsworthy about this development is that the borrowers presented a plan to the lenders in which the Related Companies would become a joint-venture partner and inject fresh capital into the project's completion. The lenders reportedly blocked this partnership in favor of taking control of the high-profile project that includes a new stadium for the New York football Giants and New York Jets, as well as the destination of the 2014 Super Bowl.

Complicated economics

What do all these developments have in common? Besides being significant events in a commercial real estate recovery, all of these otherwise newsworthy events are overshadowed by unprecedented investor obsession with the slowing economic recovery.

As a result, all eyes are on the Federal Reserve, Treasury Department, and the monthly employment numbers – more so than on commercial real estate transactions. Thus, even significant trades appear at best to be incidental events in light of Wall Street reform, and controversy over whether Fannie Mae and Freddie Mac need to be restructured.

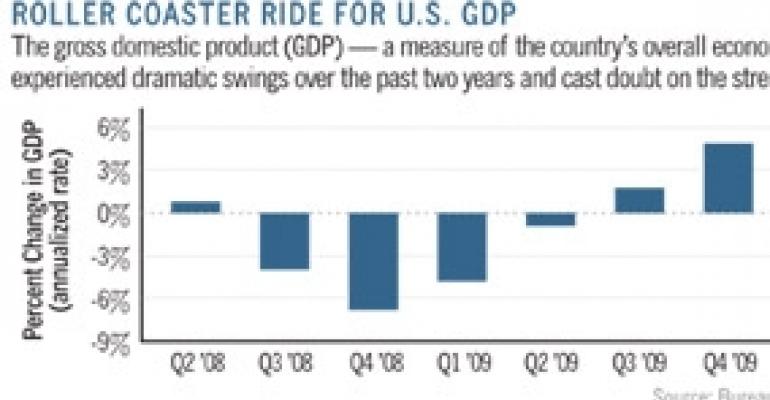

Real Gross Domestic Product (GDP) in the U.S., for instance, increased at a 2.4% annual rate for the second quarter of 2010, a figure much lower than economists had forecast. It also is the lowest reading since the third quarter of 2009, prompting pessimism and talk about a possible double-dip recession. The upshot is that growth is leveling off, and many investors, as well as skittish debt and equity providers, have taken their eye off the real estate opportunity ball.

To be sure, macroeconomics has distracted investors, as many still anxiously await the proverbial clearing price of notes and properties. The absence of banks in real estate lending has prolonged distressed loans to the point that opportunity investors such as hedge funds and private equity funds are eager to buy their way back into control of promising properties.

Buying back control

As holder of the most senior portion of the borrowers’ mezzanine debt, Pershing and Winthrop are in position to take over the equity interests in the Stuyvesant Town and Peter Cooper Village complex. This is the avenue of choice for investors on the hunt for higher tranches of mezzanine debt in struggling trophy assets.

For instance, it was the avenue used by Five Mile Capital Partners and Normandy Real Estate Partners to gain control of the John Hancock Building in Boston from Broadway Real Estate Partners. And as its junior mezzanine debt holder, LEM Mezzanine won control of the W hotel in New York at auction. LEM eventually walked away with a total repayment agreement in hand, after a high-profile battle for control of the property with Dubai World’s private equity real estate arm and its senior debt holders.

So even though this strategy is no sure bet for winning ownership of properties, it is the option most cash-rich investors are willing to pursue for now. These investors find themselves in highly competitive bidding — especially for loans — and pricing typically does not go their way. Banks, for instance, have consistently refused to sell their notes, opting instead to extend troubled loans, fully expecting better pricing down the line.

In summary, the commercial real estate recovery is moving along as well as can be expected, even though there are macroeconomic distractions along the way. As long as the Fed chairman, Treasury secretary, House Financial Services Committee, and monetary policy dominate the financial headlines, this recovery will likely be overshadowed.

The talking points among many investors today don’t revolve around opportunities that the current market presents, but instead on what the micro components of GDP mean. And investors now focus on the weekly jobless claims report, a topic they may not have had to focus on since taking Economics 101 in college.

Joe Caton is a South Florida journalist who provides training and development services to real estate finance professionals.