Real estate markets have been holding back a more robust U.S. economic recovery. Unfortunately, it is unlikely that those markets will fare much better in 2011 or even 2012. Real estate markets in the doldrums include the housing market, especially single-family homes, and the commercial property markets. This column examines both in turn to show why they are not likely to do well in 2011.

The U.S. housing market peaked in 2005 with over 2 million new units started for the second year in a row, including manufactured homes. But home builders were vastly overbuilding their markets on the wrong assumption that housing prices would always rise.

Home builders had learned nothing from past experience. New starts had always slumped badly after a year in which starts reached the level of 2 million per year. At the peak of the most recent housing boom, the number of starts actually reached 2 million two years in a row. A slump was inevitable.

Overbuilding drove home prices downward in 2006 and thereafter. Falling prices then revealed the weakness of millions of home loans made during the boom. Hence, more and more borrowers, especially with subprime mortgages, began defaulting because they falsely counted on ever-rising prices.

Home-building disaster

As a result, new home starts from 2006 through 2009 plummeted 73.2%. That plunge from 1.5 million annual starts to 554,000 — the lowest level since World War II — was the greatest housing production slump in U.S. peacetime history.

This disaster in U.S. home building and other construction drastically affected the entire economy. The number of people employed in all types of construction fell by 2.1 million from the peak in 2006 to June 2010.

That drop accounted for one-third of the total decline in private employment in all non-farming industries from 2006 to June 2010. In past recessions, housing markets usually led subsequent recoveries by rapidly increasing new starts.

However, after the sharp fall in housing starts from 1986 to 1991, it took six years for starts to regain their long-term average annual level of 1.5 million. Yet the current drop is much larger, and housing demand is being severely stifled by burgeoning foreclosures.

Foreclosures gallop on

Data firm RealtyTrac estimates that foreclosure filings were about 2.8 million in 2009 and are proceeding at a pace that could exceed 3.9 million in 2010. Hence, I believe it will take at least five more years before housing markets can return to normal conditions.

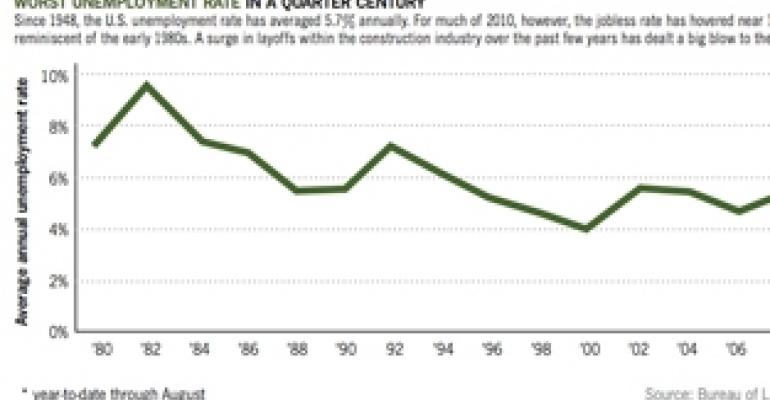

The surge in construction joblessness described above was a major reason for a sudden jump in total U.S. unemployment from under 5% in 2006 and 2007 to over 9% in 2009 and 2010. The only other time since World War II when unemployment increased nearly as fast was when it rose from 5.8% in 1979 to over 9.6% in 1982 and 1983.

That occurred when Paul Volcker raised interest rates sky-high to fight inflation. It then took four years for the unemployment rate to drop to 6%. From 2000 to June 2010, the number of people employed in all non-farming activities fell by 1.3 million, even though the number of Americans of working age (18 through 65) rose by 22 million.

This trend implies that for several more years the unemployment rate will stay much higher than its annual average of 5.7% over the 62 years from 1948 through 2010. Such a long period of high unemployment will also have adverse impacts on all types of commercial property.

True, most commercial property sectors have not suffered as much as housing because they were not as overbuilt when lending disappeared in 2007 through 2009. Yet the national office vacancy rate is now over 17%, and vacancies have also risen notably in the hotel and retail sectors as households cut back due to rising unemployment.

Debt maturities loom

But an even bigger problem in commercial markets is the overhang of huge debts coming due in the next few years. Excessive borrowing from 2000 to 2007 to finance commercial properties at low interest rates created many long-term debts on those properties coming due in the next few years. Yet most banks cannot, or will not, refinance under current pressures to deleverage their balance sheets.

Many banks, especially the smaller ones, still have overvalued real estate loans on their books that they are unwilling to sell at low market prices. They fear such cut-rate sales would reduce their net worth and might even threaten their solvency.

Hence, there is a big shortage of equity investors willing to put funds into commercial properties with big loans coming due, even though investors have several trillion dollars in hand looking for somewhere to go.

Under these conditions, real estate is not likely to lead the nation’s economy out of this recession. In fact, both the housing and commercial property markets will continue to act as a drag on U.S. economic recovery for the next several years.

Tony Downs is a senior fellow at the Brookings Institution in Washington, D.C. Contact him at [email protected].