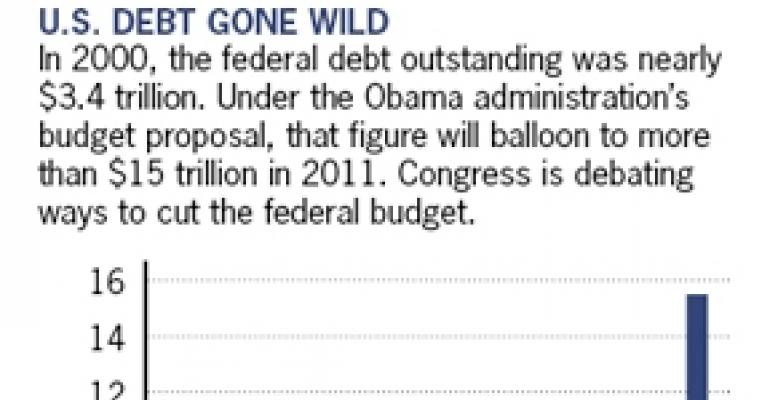

Our elected officials are at last tackling how the nation might reduce federal deficits and national debt to prevent another, even worse, financial crisis. Whatever policies are ultimately adopted will surely affect all consumers, taxpayers, and American real estate.

All Americans must face reality. We need to reduce our public and private consumption to match our incomes — something we have not done in years and are not doing now. We have to live within our means, or suffer an even worse economic collapse.

This column describes some policy requirements I believe will be necessary to reduce our standard of living to what we can afford, and some of their likely effects on real estate markets.

Debt reduction policies are necessary to escape our current financial imbalances. Federal, state, and local governments all need to reduce their total annual spending and balance their budgets.

Consumer spending as a percentage of gross domestic product (GDP) needs to decline from about 70% to 62% to reduce U.S. trade deficits. To boost government revenues, taxes need to be raised on high-income households and moderately on middle-income households.

Business taxes ought to decline to encourage more employment and investment. “Tax expenditures” that hide government spending — such as the exclusion of employer-provided health insurance from taxable income — cost more than $500 billion per year and should be drastically reduced.

Reducing the roles of Fannie Mae and Freddie Mac in housing would raise mortgage interest rates. Mortgage interest deductions for homeowners ought to be slashed or changed to fixed tax credits to reduce current subsidies that mainly benefit high-income homeowners.

If the Federal Reserve stops pumping money into the economy when Quantitative Easing 2 expires at the end of June, that will reduce upward pressure on many prices, though some inflation will still occur.

No overall means of reducing home foreclosures will happen. The federal government cannot finance them and lenders will not accept haircuts to keep occupants in their homes. So many more foreclosures will continue to handicap home markets.

Likely impact of such policies

Lower government spending means fewer new roads and transit systems, and less maintenance of existing roads, bridges and railroad tracks. Gasoline taxes are inadequate to maintain our highways, but there is no political will to raise them.

So financing of surface transportation beyond the gas tax will devolve to state and local governments. Expect more private ownership of freeways and other means of transportation.

Lower consumer spending means the percentage of households who can afford buying homes will decline. Demand for rental housing is already rising compared to demand for new homes. Many more smaller, lower-cost homes will be built.

Retail spending should grow more slowly than overall incomes as households try to offset higher unemployment, higher tax rates, and fewer reductions in retail prices through imports.

Reduced consumption spending will adversely affect all retail and shopping businesses. Construction of new retail outlets will remain low, and many existing outlets will close or be converted to other uses.

Office occupancy by government agencies will decline, especially affecting downtown areas. High gasoline prices will cause more workers to telecommute, somewhat reducing the demand for office space and shifting to smaller office spaces per worker.

Domestic travel may increase in spite of higher gasoline prices because foreign travel will be more costly than ever. Hotels and resorts outside the U.S. will get less American patronage, but more patronage from emerging nations.

If Congress and the President drastically cut government spending and debt, real estate will experience many negative consequences, but will slowly recover as will most businesses.

Unfortunately, too many groups will keep demanding benefits that they will not pay for, except through more borrowing. That will plunge our nation into a worse financial crisis.