It is no secret that a number of metropolitan areas in the south and west have benefited significantly from the recent oil and gas drilling boom. Metro GDP data for 2014 recently released from the Bureau of Economic Analysis shows a broad range in growth rates across the country. The metro areas that saw the highest growth rates were the same ones that saw the sharpest apartment rent growth for the same period.

While technology-focused economies such as San Francisco and San Jose were among the top 10 metros, the remaining high-growth metros were those fueled by drilling-related business.

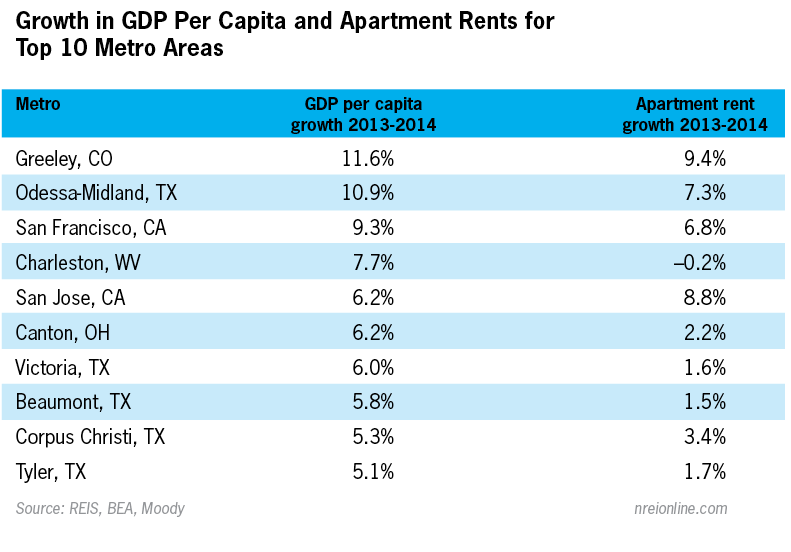

The top two markets, Greeley, Colo. and Midland-Odessa, Texas posted metro GDP per capita growth rates of 11.6 percent and 10.9 percent respectively. Greeley has seen a sizable jump in both oil and gas drilling in the Denver-Julesburg basin that cuts across the northeast corner of the state. Odessa-Midland’s growth came from drilling in the Permian basin. Both areas saw strong energy-related job growth in a short time period. Greeley’s “natural resources and mining” industry added 2,525 jobs in one year, a growth rate of 25 percent. These added jobs accounted for 9 percent of the overall job growth in Greeley county. In Odessa-Midland, the mining industry grew by 14 percent from 2013 to 2014, accounting for 40 percent of the total job growth in the metro.

All of these added jobs put considerable upward pressure on rent growth. Greeley saw its apartment rents grow by 9.4 percent, while Odessa-Midland saw rents grow by 7.3 percent from 2013 to 2014.

Rounding out the top five metros, San Francisco and San Jose recorded per capita GDP growth rates of 9.3 percent and 6.2 percent respectively, in line with apartment rent growth rates of 6.8 percent and 8.8 percent.

Oddly, Charleston, W.V. had a high GDP growth rate due partially to a drop in population. This town was ground zero for the Elk River Chemical spill in early 2014. Not surprisingly, apartment rents in Charleston declined by 0.2 percent in 2014.

A number of other smaller metros posted high GDP and rent growth rates such as Canton, Ohio, Victoria, Beaumont, Corpus Christi and Tyler, Texas. These markets saw one-year per capita GDP growth rates above 5 percent, but only Corpus Christi had rent growth above 3 percent. Job growth in these areas was noteworthy, but not strong enough to make an impact on rents.

But other, larger metros with high growth were Denver and Dallas, again, with drilling-driven growth. Both Dallas and Denver saw GDP growth rates of 4.5 percent, and apartment rent growth of 7.5 percent (Denver) and 4.6 percent (Dallas).

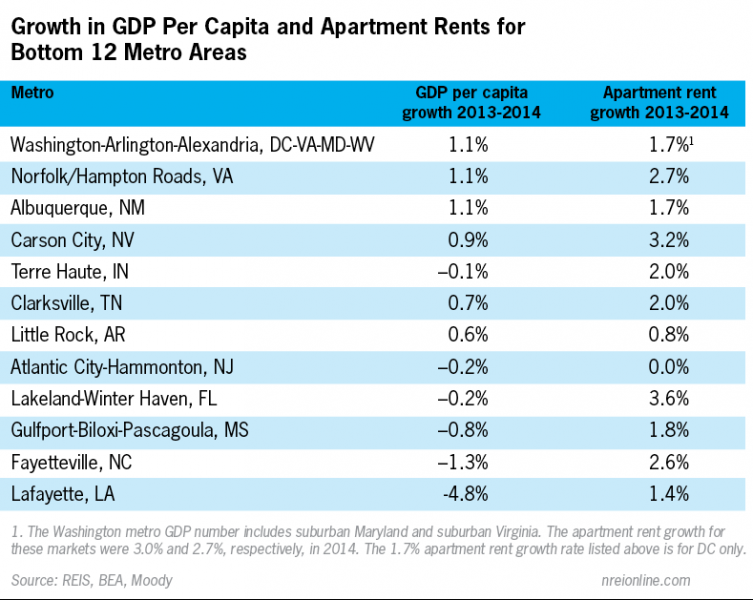

At the bottom, metros with the weakest growth included Camden, N.J., Little Rock, Ark., Virginia Beach-Norfolk, Va., Albuquerque, N.J. and Washington, D.C. These markets all had GDP growth of less than 1.2 percent and rent growth of 1.7 percent and below. The market with the lowest growth was Lakeland, La., whose offshore drilling businesses suffered from the industry shift towards fracking in the basins listed above. Lakeland’s per capita GDP fell 4.8 percent from 2013 to 2014. The next lowest was Fayetteville, N.C., which saw a decline of only 1.3 percent.

While these statistics confirm the overwhelming economic impact of the drilling industry, the obvious question emerges: how sharply have these and other markets been hit by the drop in oil prices since the start of 2015?

The short answer so far is: very little. Reis data shows that the drop in oil prices has had little to no impact on rent growth. Dallas and Denver saw year-over-year rent growth rates of 4.7 percent and 6.9 percent respectively, as of the third quarter. Houston’s year-over-year growth rate was 4.1 percent and its vacancy rate was unchanged in the quarter at 5.0 percent. Dallas and Denver’s vacancy rates were just under 5.0 percent. But these are large metropolitan areas with diverse economies. How have some of the tertiary markets fared in 2015, particularly the ones mentioned above?

Oddly enough, Greeley continued to see remarkable rent growth in 2015, rising 6.5 percent year-over-year. Odessa-Midland’s rents have grown 3.0 percent in 2015. At the other end, Lakeland rents declined 0.3 percent in 2015, after increasing 1.4 percent in 2014. Clearly, the impact from reduced offshore drilling hit Lakeland’s apartment market with a lag. The Texas tertiary markets saw rent growth ranging from 0.2 percent (Beaumont) to 3.3 percent (Corpus Christi). In other words, the shale-based markets are surviving relatively unscathed thus far, but as mentioned, these impacts tend to hit with a lag.

The outlook on the oil market is still unclear. Many have expressed concern for these markets where shale fracking has spurred so much growth. But some of the fracking in these basins is for natural gas, which serves as an alternative to oil in some capacity (heating), yet it competes with different market forces and regulatory issues. In short, it is too early to tell how lower oil prices will impact these markets. Capturing per capita GDP growth numbers was a worthy exercise not only to compare to Reis rent data, but it yielded data on these outlying metros. More importantly, because economic shifts precede real estate changes, this metro-level GDP data serves as a lead variable to real estate performance. Revisiting these GDP growth figures a year from now should reinforce this determination. Until then, we can keep a close eye on rents to see how these markets are faring.

Barbara Byrne Denham and Victor Calanog are economists at Reis, Inc, a provider of commercial real estate data and analytics.