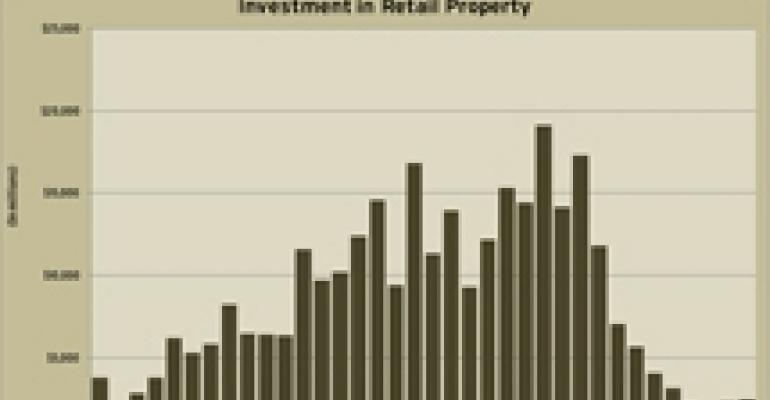

As the industry tallies the final numbers on sales activity in 2009, the consensus is that last year marked a long-term low point in transaction volume. According to preliminary figures from Real Capital Analytics (RCA), a New York City-based research firm, there were approximately $10.5 billion to $11 billion in retail investment sales completed in 2009—about one-fifth the $62 billion in retail property sales that occurred in 2007. In fact, the full year volume for 2009 was lower than any quarter of 2007. The volume is in line with what occurred in 2001, when $12.3 billion in retail investment sales activity took place.

The last three months of 2009, however, did bring an uptick in new sales and hope that 2010 might prove to be marginally better. Among the notable transactions that occurred was North Miami Beach, Fla.-based REIT Equity One Inc.’s acquisition of 400,000-square-foot Westbury Plaza in Nassau County, N.Y. from Kimco Realty Corp. and DRA Advisors for $103.7 million. Meanwhile, Pacific Retail Capital Partners, a Los Angeles-based private investment firm, bought the 1.1-million-square-foot West Oaks Mall in Houston from special servicer LNR Partners for $15 million.

In November, sales of significant retail properties totaled $711 million, down 30 percent from November 2008, according to RCA. From Dec. 1 through Dec. 22, RCA counted $340 million in closed transactions, plus more deals that were under contract. And that doesn’t take into account Simon Property Group’s $2.3 billion deal to acquire Prime Outlets Acquisition Co. That deal, by itself, is larger than any of the quarters from 2009, but won’t be reflected in RCA’s numbers until the deal closes.

The reasons for the increase in activity include the narrowing of the bid-ask gap between buyers and sellers and the desire by many owners to deleverage, says Bernard J. Haddigan, senior vice president and managing director of the national retail group with Marcus & Millichap Real Estate Investment Services, an Encino, Calif.-based brokerage firm. “There are a lot of people who are looking to do things,” he notes. “Those on the offensive are asking ‘How can I get some cheap real estate that’s very stable?’ Defensively, people are looking to sell [to pay down debt]. People coming out of this cycle are going to embrace low leverage for quite some time.”

The problem is that most of the buyers currently in the market are interested only in value-add or core assets—fully occupied grocery-anchored shopping centers in primary markets, with credit tenants, says Anthony F. Buono, executive managing director of retail services for the Americas with CB Richard Ellis, a global real estate services firm. Historically, these kinds of assets make up only a fraction of the retail marketplace and owners in possession of core properties today would probably opt to hold onto them if possible.

In fact, the relative scarcity of supply in this product group has led to a slight decrease in cap rates in the third and fourth quarters of 2009, according to a December report compiled by Philip D. Voorhees, senior vice president with CBRE’s national retail investment group-West. Cap rates on core assets valued at more than $20 million declined 25 basis points to 50 basis points during that period, to the high 7 percent range.

Smaller, free-standing properties leased to good credit tenants also remain in demand, according to Haddigan. He estimates, for example, that a McDonald’s ground lease in a primary market can still trade at a 6 percent cap rate.

Remaining asset classes, however, continue to be viewed skeptically by risk-wary buyers. Investors remain concerned about falling rental rates and possible tenant bankruptcies, according to Voorhees’ report, especially given that this year’s holiday shopping season was far from a wild success. Plus, though the credit markets began to thaw in the second half of 2009, securing acquisition financing remains a challenge for many buyers, says Buono. He expects that in 2010, the acquisition market will be made up primarily of private capital and private REITs such as Phoenix, Ariz.-based Cole Real Estate Investments. The company remained an active investor throughout 2009, purchasing at least 107 properties valued at $522 million.

Still, with all the cash sitting on the sidelines and the perception that the worst of the downturn may be over, at least when it comes to the impact on retailers, 2010 should prove to be a better year for investment sales than 2009, according to Buono.

“If you look at 2002 or 2003 and transaction volume in the overall market, you can say ‘It’s a re-emerging market,’” he notes. “It wasn’t wild like 2006, but it wasn’t as draconian as 2009. It was kind of a coming-out period.”

In 2002, RCA reported $25.5 billion in retail investment sales, followed by $30.7 billion in 2003.

—Elaine Misonzhnik