In spite of a wobbly job market and falling housing prices, the retail real estate sector is recovering. The retail vacancy rate in the first quarter stood at 7.1%, according to the CoStar Group, a Washington, D.C.-based research firm, in line with the fourth quarter of 2010.

However, asking rents in the first quarter fell to $14.86 per sq. ft., from $14.91 at the end of 2010, reports CoStar.

“[We] believe that rents coming back to pre-recession levels is still two to three years away,” says Naveen Jaggi, senior managing director in the Houston office of brokerage giant CB Richard Ellis. “Until then, the creditworthiness of the tenants will drive most deals.”

Extra perks

The good news for landlords is that the days of every tenant asking for rent concessions have passed.

That said, national retail tenants with strong credit ratings know they are rare enough to demand generous tenant improvement packages, shorter-than-average leases, and caps on common area maintenance (CAM) charges from landlords.

“There is still a lot of uncertainty with existing tenants and still a lot of changes in vacancy happening in the marketplace,” says Branson Edwards, Chicago-based executive vice president with Grubb & Ellis.

“It seems to us that we are still some time away from there being parity between tenants and landlords,” he adds.

For example, a national retailer signing a lease for a 25,000 sq. ft. former Circuit City box will ask for anywhere from $40 to $60 per sq. ft. in TI and a base rent that can be as low as $10 per sq. ft.

In addition, the new tenant will likely want a termination clause if sales don't reach desired levels within a three-year period, according to Gene Spiegelman, executive vice president in the New York office of Cushman & Wakefield.

“If I were the retailer, I'd be looking to come in, turn on the lights, and if the situation warranted, leave in two or three years.”

There are exceptions, however. Owners of Class-A malls are in a strong enough position that they no longer have to meet every demand from tenants, according to Spiegelman, because vacancy at those properties has come back to historical levels.

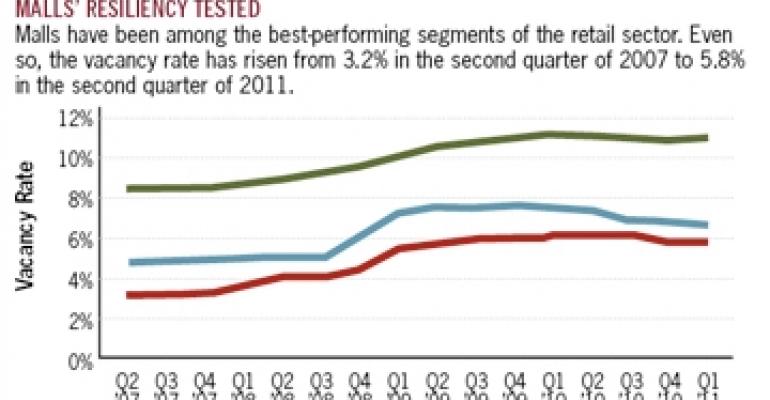

At the end of first quarter, vacancy at regional malls nationwide stood at 5.8%, according to CoStar, lower than most other retail property types (see chart).

Landlords at better performing properties are pushing back against requests for shorter lease terms. If a retailer gets a TI allowance, the landlord will ask for a 10-year term, with a five-year option, according to Jaggi. Previously, many retailers would insist on signing three- and five-year leases.

The right prices

The investment sales market for retail properties also is heating up as buyers gain more confidence in the economy and financing has become easier to obtain.

In April, sales of retail properties valued above $2.5 million reached $1.6 billion — a year-over-year increase of 39%, according to Real Capital Analytics (RCA).

Year-to-date through April, the market notched $7.9 billion in completed deals and another $16 billion in pending transactions. In contrast, through the first four months of 2010, the market saw $4.1 billion in completed deals.

What's more, investors no longer limit themselves to Class-A product in primary markets, says Bill Rose, national director of the retail group at Marcus & Millichap Real Estate Investment Services based in Encino, Calif.

The investment sales market “is mirroring the capital markets and the capital markets are now open to financing Class-B and Class-C properties,” says Rose.

“We are seeing a substantial uptick in multi-tenant transactions, in deals north of $5 million. We are going to be awfully busy this summer and fall,” predicts Rose.

As a result of improving market conditions, average cap rates on retail acquisitions fell to 7.5% in April, according to RCA, 20 basis points below the 7.7% recorded in January.

CLICK BELOW TO SEE: