A significant percentage of investors prefer to place their money in large cap REITs, choosing the security of bigger companies and often ignoring small cap REITs completely.

That decision is short sighted, experts say.

Today’s large cap REITs were—at one point—small cap players that achieved success and size over time. Some analysts suggest that investors should view today’s small cap REITs as tomorrow’s giants. This will provide opportunities to generate returns as small cap REITs grow into larger, more successful companies.

“In my view, current market cap is not a primary determinant of future value creation,” says James Milam, a REIT analyst with Sandler O’Neill + Partners L.P. “It’s worth pointing out that the REITs that lead the sector in terms of market capitalization today didn’t IPO at those sizes. REITs with good management teams and good strategies, regardless of their market cap, are going to find a way to make money for their investors.”

While Milam acknowledges that large cap REITs may have some advantages over small cap REITs—liquidity, access to capital and cost of capital—he warns against making investment decisions based solely on size. With that said, it’s hard to argue with the performance that large cap REITs have achieved over the past five years.

To offer some perspective on the REIT sector overall, the largest REIT is Simon Property Group at $53.4 billion, while micro REITs such as Tower REIT and Pacific Office Properties Trust Inc. have market caps of right around $2 million. Many of the small and micro cap REITs also don’t trade on the New York Stock Exchange, but through over the counter markets.

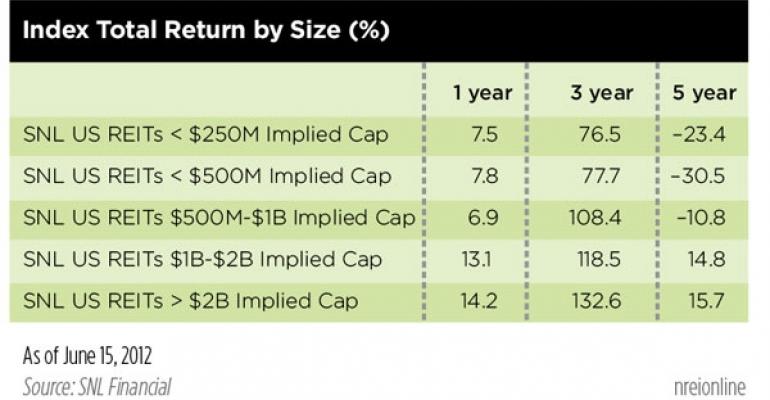

When looking at total returns, large cap REITs have delivered more impressive than returns small cap REITs. For example, over a five-year period through mid-June, large cap REITs (those over $2 billion in market cap), posted a total return of 15.7 percent compared to -23.4 percent for REITs with a market cap less than $250 million, according to SNL Financial.

It’s worth nothing, however, that dividend yields for smaller cap REITs are heftier than for larger cap REITs. In most instances, the smaller the market cap, the larger the dividend yield.

Simon, for example has a current dividend yield of 2.68 percent. In contrast, Atlanta-based Preferred Apartment Communities Inc., which has a market cap of roughly $37 million, boasts a dividend yield of 7.22 percent.

“The flow of funds into large cap REITs is driving up the prices of these companies, decreasing their price to earnings and driving down yields,” says Adam Patti, CEO of IndexIQ, which manages several ETFs including IQ US Real Estate Small Cap ETF (ROOF), the only small cap REIT Index in the nation. He points to ROOF’s dividend yield of 7.69 percent versus 3.33 percent for the Bloomberg Real Estate Investment Trust Large Cap Index (BBRELRGC).

Another large cap REIT drawback is increased correlation and volatility with the broader market.

“Large market cap REITs are often part of larger indexes, and as a result, they’re more volatile and correlated with the market,” Patti points out. He adds that he’s not advocating that investors eschew large cap REITs, but simply that they allocate a portion of their funds to small cap players as well.

Certainly, Patti is an unashamed and vocal proponent of small cap REITs, but he is quick to make the distinction between small and micro-cap. For example, ROOF’s median invested REIT is $884 million with the largest market cap company at roughly $2 billion.

In constructing ROOF, Patti and his team made sure to create market cap criteria that would ensure liquidity for investors. Not only did the company cut out companies with a market cap less than $150 million, it also limited the pool of potential REITs to those with at least $1 million in daily trades and/or 250,000 shares.

“Those really small REITs are not usually the best way to go,” Patti opines. “More often than not, they’re undercapitalized, and they could be cheap for a reason.”