Leasing activity may be experiencing a renaissance if retail landlords are to be believed, but it’s still taking a while for property fundamentals to return to historically healthy levels.

One only has to look at retail REITs’ recent performance to see that the market has taken a turn for the better. For instance, mall operator Simon Property Group reported a 110 basis point increase in portfolio occupancy from the first quarter of 2012 to the first quarter of 2013, to 94.7 percent. Base minimum rent per sq. ft. went up 3 percent, to $41.05.

Shopping center operator Kimco Realty Corp. reported that pro-rate occupancy within its portfolio rose 70 basis points during the same period, to 93.6 percent.

During the first quarter of 2013, the average vacancy rate at all neighborhood and community shopping centers declined by 30 basis points compared to the same period in 2012, to 10.6 percent, according to Reis Inc., a New York City-based research firm. Effective rents rose 0.7 percent year-over-year, to $19.13 per sq. ft.

That will likely remain the pace of improvement for the next two years as the country deals with the impact of the sequestration and increased taxation rates, according to Ryan Severino, Reis’ senior economist. Consumers are still worried about debt and while the housing market has started on the path to recovery, the process will take a while to complete.

“We are still talking about marginal improvement,” he says about the first quarter numbers. “We really have to get into the middle of this decade before we start to see anything substantial.”

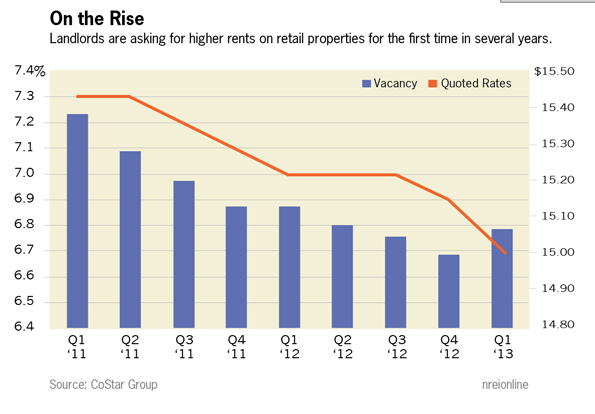

The CoStar Group, a Washington, D.C.-based research firm that tracks fundamentals at all retail properties, reported an equally modest decline in overall vacancy since the first quarter of 2012—by 30 basis points, to 6.7 percent. That’s in spite of the fact that new construction deliveries have been minimal last year, at 47.6 million sq. ft. During the peak of the previous cycle the industry delivered more than 200 million sq. ft. of new retail space a year.

Shopping centers as a group had an average vacancy rate of 10.4 percent, representing a 40 basis point decline from the first quarter of 2012, according to CoStar. Regional and superregional malls, on the other hand, had a 5.9 percent vacancy rate—flat with the year prior.

Reason for optimism

The good news, according to Ryan McCullough, real estate economist with CoStar, is that retail properties are now showing rent growth for the first time since 2008. In the first quarter, average quoted rates for all retail properties stood at $15.07 per sq. ft., an improvement over $15.08 per sq. ft. a year ago and $15.00 per sq. ft. in the fourth quarter of 2012.

“This rent bump is a sign that the market is finally reaching some degree of equilibrium after two and a half years of slow, but steady recovery,” McCullough says.

Driving the higher rents is greater consumer confidence and continuing recovery in the housing sector, according to first quarter report by real estate services firm Colliers International. Colliers reports that at shopping centers, asking rents rose $0.03 per sq. ft. between the fourth quarter of 2012 and the first quarter of 2013, to $14.80 per sq. ft.

In fact, once the major issues created by the recession—including the housing bust—will finally get worked out, the retail real estate industry can expect quite a strong comeback, notes Severino.

“By 2014-2015, you’ll see the economy in a much better place, a lot of the debt overhang that we are dealing with will be resolved,” he says. “Assuming that we don’t end up with some massive idiosyncratic shock to the system, we’ll be in a much better position.”